Exhibit 99.1 P3 Analyst Day Presentation September 2021 Who: People with Passion and Purpose What: Dedicated to Transforming Healthcare for Patients, Providers, and Payors How: Patient-Centric, Physician-Led, and Population Health Management FocusedExhibit 99.1 P3 Analyst Day Presentation September 2021 Who: People with Passion and Purpose What: Dedicated to Transforming Healthcare for Patients, Providers, and Payors How: Patient-Centric, Physician-Led, and Population Health Management Focused

Disclaimer BASIS OF PRESENTATION This presentation is provided for informational purposes only and has been prepared to assist interested parties in making their own evaluation with respect to a potential business combination (the “proposed business combination”) between P3 Health Partners (“P3”) and Foresight Acquisition Corp. (“Foresight” or “SPAC”), and related transactions, and for no other purpose. No representations or warranties, express or implied are given in, or in respect of, this presentation. To the fullest extent permitted by law, in no circumstances will P3, Foresight or any of their respective subsidiaries, stockholders, affiliates, representatives, partners, directors, officers, employees, advisers or agents be responsible or liable for any direct, indirect or consequential loss or loss of profit arising from the use of this presentation, its contents, its omissions, reliance on the information contained within it, or on opinions communicated in relation thereto or otherwise arising in connection therewith. Industry and market data used in this presentation have been obtained from third party industry publications and sources. None of P3 or Foresight has independently verified the data obtained from these sources and cannot assure you of the data’s accuracy or completeness. This data is subject to change. In addition, this presentation does not purport to be all-inclusive or to contain all of the information that may be required to make a full analysis of P3 or the proposed business combination. Recipients of this presentation should each make their own evaluation of P3 and of the relevance and adequacy of the information and should make such other investigations as they deem necessary. FORWARD-LOOKING STATEMENTS Any investment in or purchase of any securities of P3 or Foresight is speculative and involves a high degree of risk and uncertainty. This presentation includes “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements may be identified by the use of words such as “estimate,” “plan,” “project,” “forecast,” “intend,” “will,” “expect,” “anticipate,” “believe,” “seek,” “target” or other similar expressions that predict or indicate future events or trends or that are not statements of historical matters. These forward-looking statements include, but are not limited to, statements regarding estimates and forecasts of financial and performance metrics, projections of market opportunity and market share, expectations and timing related to site build-outs and capacity deployment, potential benefits of the transaction and the potential success of P3's strategy and expectations related to the terms and timing of the proposed business combination and related transactions. These statements are based on various assumptions, whether or not identified in this presentation, and on the current expectations of P3’s and Foresight’s management and are not predictions of the actual performance. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. Many actual events and circumstances are beyond the control of P3 and Foresight. These forward-looking statements are subject to a number of risks and uncertainties, including changes in domestic and foreign business, market, financial, political, legal and regulatory conditions; the inability of the parties to successfully or timely consummate the proposed business combination, including the risk that the conditions to the proposed business combination are not satisfied or waived, including that any required regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could adversely affect the combined company or the expected benefits of the proposed business combination or that the approval of the stockholders of Foresight is not obtained; failure to realize the anticipated benefits of the proposed business combination; risks related to the effects and uncertainties created by the ongoing COVID-19 pandemic; risks relating to the uncertainty of the projected financial information with respect to P3; risks related to the rollout of P3’s business and the timing of expected business milestones; risks related to P3’s commercial partnerships, including the inability of P3 and commercial counterparties to enter into definitive agreements; future global, regional or local economic and market conditions; the development, effects and enforcement of laws and regulations; P3’s ability to manage future growth; P3’s ability to develop new products and solutions, bring them to market in a timely manner, and make enhancements to its platform; the effects of competition on P3’s future business; the amount of redemption requests made by Foresight’s public stockholders; the ability of Foresight or the combined company to issue equity or equity-linked securities in connection with the proposed business combination or in the future; the outcome of any potential litigation, government and regulatory proceedings, investigations and inquiries; and those factors discussed in Foresight’s Annual Report on Form 10-K for the year ended December 31, 2020 and filed with the SEC on April 6, 2021 (the “Annual Report”) under the heading “Risk Factors,” Preliminary Proxy Statement on Schedule 14A filed with the SEC on August 12, 2021 under the heading “Risk Factors,” and other documents of Foresight filed, or to be filed, with the SEC. If any of these risks materialize or our assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. There may be additional risks that neither Foresight nor P3 presently know or that Foresight and P3 currently believe are immaterial that could also cause actual results to differ from those contained in the forward- looking statements. In addition, forward-looking statements reflect Foresight’s and P3’s expectations, plans or forecasts of future events and views as of the date of this presentation. Foresight and P3 anticipate that subsequent events and developments will cause Foresight’s and P3’s assessments to change. However, while Foresight and P3 may elect to update these forward-looking statements at some point in the future, Foresight and P3 specifically disclaim any obligation to do so. These forward-looking statements should not be relied upon as representing Foresight’s and P3’s assessments as of any date subsequent to the date of this presentation. Accordingly, undue reliance should not be placed upon the forward- looking statements. 1Disclaimer BASIS OF PRESENTATION This presentation is provided for informational purposes only and has been prepared to assist interested parties in making their own evaluation with respect to a potential business combination (the “proposed business combination”) between P3 Health Partners (“P3”) and Foresight Acquisition Corp. (“Foresight” or “SPAC”), and related transactions, and for no other purpose. No representations or warranties, express or implied are given in, or in respect of, this presentation. To the fullest extent permitted by law, in no circumstances will P3, Foresight or any of their respective subsidiaries, stockholders, affiliates, representatives, partners, directors, officers, employees, advisers or agents be responsible or liable for any direct, indirect or consequential loss or loss of profit arising from the use of this presentation, its contents, its omissions, reliance on the information contained within it, or on opinions communicated in relation thereto or otherwise arising in connection therewith. Industry and market data used in this presentation have been obtained from third party industry publications and sources. None of P3 or Foresight has independently verified the data obtained from these sources and cannot assure you of the data’s accuracy or completeness. This data is subject to change. In addition, this presentation does not purport to be all-inclusive or to contain all of the information that may be required to make a full analysis of P3 or the proposed business combination. Recipients of this presentation should each make their own evaluation of P3 and of the relevance and adequacy of the information and should make such other investigations as they deem necessary. FORWARD-LOOKING STATEMENTS Any investment in or purchase of any securities of P3 or Foresight is speculative and involves a high degree of risk and uncertainty. This presentation includes “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements may be identified by the use of words such as “estimate,” “plan,” “project,” “forecast,” “intend,” “will,” “expect,” “anticipate,” “believe,” “seek,” “target” or other similar expressions that predict or indicate future events or trends or that are not statements of historical matters. These forward-looking statements include, but are not limited to, statements regarding estimates and forecasts of financial and performance metrics, projections of market opportunity and market share, expectations and timing related to site build-outs and capacity deployment, potential benefits of the transaction and the potential success of P3's strategy and expectations related to the terms and timing of the proposed business combination and related transactions. These statements are based on various assumptions, whether or not identified in this presentation, and on the current expectations of P3’s and Foresight’s management and are not predictions of the actual performance. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. Many actual events and circumstances are beyond the control of P3 and Foresight. These forward-looking statements are subject to a number of risks and uncertainties, including changes in domestic and foreign business, market, financial, political, legal and regulatory conditions; the inability of the parties to successfully or timely consummate the proposed business combination, including the risk that the conditions to the proposed business combination are not satisfied or waived, including that any required regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could adversely affect the combined company or the expected benefits of the proposed business combination or that the approval of the stockholders of Foresight is not obtained; failure to realize the anticipated benefits of the proposed business combination; risks related to the effects and uncertainties created by the ongoing COVID-19 pandemic; risks relating to the uncertainty of the projected financial information with respect to P3; risks related to the rollout of P3’s business and the timing of expected business milestones; risks related to P3’s commercial partnerships, including the inability of P3 and commercial counterparties to enter into definitive agreements; future global, regional or local economic and market conditions; the development, effects and enforcement of laws and regulations; P3’s ability to manage future growth; P3’s ability to develop new products and solutions, bring them to market in a timely manner, and make enhancements to its platform; the effects of competition on P3’s future business; the amount of redemption requests made by Foresight’s public stockholders; the ability of Foresight or the combined company to issue equity or equity-linked securities in connection with the proposed business combination or in the future; the outcome of any potential litigation, government and regulatory proceedings, investigations and inquiries; and those factors discussed in Foresight’s Annual Report on Form 10-K for the year ended December 31, 2020 and filed with the SEC on April 6, 2021 (the “Annual Report”) under the heading “Risk Factors,” Preliminary Proxy Statement on Schedule 14A filed with the SEC on August 12, 2021 under the heading “Risk Factors,” and other documents of Foresight filed, or to be filed, with the SEC. If any of these risks materialize or our assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. There may be additional risks that neither Foresight nor P3 presently know or that Foresight and P3 currently believe are immaterial that could also cause actual results to differ from those contained in the forward- looking statements. In addition, forward-looking statements reflect Foresight’s and P3’s expectations, plans or forecasts of future events and views as of the date of this presentation. Foresight and P3 anticipate that subsequent events and developments will cause Foresight’s and P3’s assessments to change. However, while Foresight and P3 may elect to update these forward-looking statements at some point in the future, Foresight and P3 specifically disclaim any obligation to do so. These forward-looking statements should not be relied upon as representing Foresight’s and P3’s assessments as of any date subsequent to the date of this presentation. Accordingly, undue reliance should not be placed upon the forward- looking statements. 1

Disclaimer USE OF PROJECTIONS AND DESCRIPTION OF KEY CONTRACTS AND PARTNERSHIPS This presentation contains projected financial information with respect to P3, namely revenue and EBITDA for 2021. Such projected financial information constitutes forward-looking information, and is for illustrative purposes only and should not be relied upon as necessarily being indicative of future results. The assumptions and estimates underlying such projected financial information are inherently uncertain and are subject to a wide variety of significant business, economic, competitive and other risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information. See “Forward-Looking Statements” above. Actual results may differ materially from the results contemplated by the projected financial information contained in this presentation, and the inclusion of such information in this presentation should not be regarded as a representation by any person that the results reflected in such projections will be achieved. Neither the independent auditors of Foresight nor the independent auditors of P3, audited, reviewed, compiled, or performed any procedures with respect to the projections for the purpose of their inclusion in this presentation, and accordingly, neither of them expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this presentation. This presentation contains descriptions of certain key business partnerships of P3. These descriptions are based on the P3 management team’s discussions with such counterparties and the latest available information and estimates as of the date of this presentation. In each case, such descriptions are subject to negotiation and execution of definitive agreements with such counterparties which have not been completed as of the date of this presentation and, as a result, such descriptions of key business partnerships of P3, remain subject to change FINANCIAL INFORMATION; NON-GAAP FINANCIAL MEASURES The financial information and data contained in this presentation is unaudited and does not conform to Regulation S-X. Accordingly, such information and data may not be included in, may be adjusted in or may be presented differently in, any proxy statement, registration statement, or prospectus to be filed by Foresight with the SEC. Some of the financial information and data contained in this presentation, such as EBITDA and EBITDA Margin have not been prepared in accordance with United States generally accepted accounting principles (“GAAP”). EBITDA is defined as net earnings (loss) before interest expense, income tax expense (benefit), depreciation and amortization. Foresight and P3 believe these non-GAAP measures of financial results provide useful information to management and investors regarding certain financial and business trends relating to P3’s financial condition and results of operations. Foresight and P3 believe that the use of these non-GAAP financial measures provides an additional tool for investors to use in evaluating projected operating results and trends in and in comparing P3’s financial measures with other similar companies, many of which present similar non-GAAP financial measures to investors. Management does not consider these non-GAAP measures in isolation or as an alternative to financial measures determined in accordance with GAAP. The principal limitation of these non-GAAP financial measures is that they exclude significant expenses and income that are required by GAAP to be recorded in P3’s financial statements. In addition, they are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non-GAAP financial measures. P3 is not providing a reconciliation of its projected EBITDA, EBITDA Margin and other metrics for full years 2021-2025 to the most directly comparable measure prepared in accordance with GAAP because P3 is unable to provide this reconciliation without unreasonable effort due to the uncertainty and inherent difficulty of predicting the occurrence, the financial impact, and the periods in which the adjustments may be recognized. For the same reasons, P3 is unable to address the probable significance of the unavailable information, which could be material to future results. ADDITIONAL INFORMATION ABOUT THE PROPOSED BUSINESS COMBINATION AND WHERE TO FIND IT The proposed business combination will be submitted to stockholders of Foresight for their consideration. Foresight filed preliminary a proxy statement (the “Proxy Statement”) with the SEC on August 12, 2021. After the definitive Proxy Statement has been filed, Foresight will mail the definitive Proxy Statement and other relevant documents to its stockholders as of the record date established for voting on the proposed business combination. Foresight's stockholders and other interested persons are advised to read, once available, the preliminary Proxy Statement and any amendments thereto and, once available, the definitive Proxy Statement, in connection with Foresight's solicitation of proxies for its special meeting of stockholders to be held to approve, among other things, the proposed business combination, because these documents will contain important information about Foresight, P3 and the proposed business combination. Investors and securities holders may also obtain a copy of the preliminary or definitive Proxy Statement, once available, as well as other documents filed with the SEC regarding the proposed business combination and other documents filed with the SEC by Foresight, without charge, at the SEC's website located at www.sec.gov or by directing a request to Gateway Investor Relations, (949) 574-3860, FORE@gatewayir.com. INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED OR DISAPPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE. 2Disclaimer USE OF PROJECTIONS AND DESCRIPTION OF KEY CONTRACTS AND PARTNERSHIPS This presentation contains projected financial information with respect to P3, namely revenue and EBITDA for 2021. Such projected financial information constitutes forward-looking information, and is for illustrative purposes only and should not be relied upon as necessarily being indicative of future results. The assumptions and estimates underlying such projected financial information are inherently uncertain and are subject to a wide variety of significant business, economic, competitive and other risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information. See “Forward-Looking Statements” above. Actual results may differ materially from the results contemplated by the projected financial information contained in this presentation, and the inclusion of such information in this presentation should not be regarded as a representation by any person that the results reflected in such projections will be achieved. Neither the independent auditors of Foresight nor the independent auditors of P3, audited, reviewed, compiled, or performed any procedures with respect to the projections for the purpose of their inclusion in this presentation, and accordingly, neither of them expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this presentation. This presentation contains descriptions of certain key business partnerships of P3. These descriptions are based on the P3 management team’s discussions with such counterparties and the latest available information and estimates as of the date of this presentation. In each case, such descriptions are subject to negotiation and execution of definitive agreements with such counterparties which have not been completed as of the date of this presentation and, as a result, such descriptions of key business partnerships of P3, remain subject to change FINANCIAL INFORMATION; NON-GAAP FINANCIAL MEASURES The financial information and data contained in this presentation is unaudited and does not conform to Regulation S-X. Accordingly, such information and data may not be included in, may be adjusted in or may be presented differently in, any proxy statement, registration statement, or prospectus to be filed by Foresight with the SEC. Some of the financial information and data contained in this presentation, such as EBITDA and EBITDA Margin have not been prepared in accordance with United States generally accepted accounting principles (“GAAP”). EBITDA is defined as net earnings (loss) before interest expense, income tax expense (benefit), depreciation and amortization. Foresight and P3 believe these non-GAAP measures of financial results provide useful information to management and investors regarding certain financial and business trends relating to P3’s financial condition and results of operations. Foresight and P3 believe that the use of these non-GAAP financial measures provides an additional tool for investors to use in evaluating projected operating results and trends in and in comparing P3’s financial measures with other similar companies, many of which present similar non-GAAP financial measures to investors. Management does not consider these non-GAAP measures in isolation or as an alternative to financial measures determined in accordance with GAAP. The principal limitation of these non-GAAP financial measures is that they exclude significant expenses and income that are required by GAAP to be recorded in P3’s financial statements. In addition, they are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non-GAAP financial measures. P3 is not providing a reconciliation of its projected EBITDA, EBITDA Margin and other metrics for full years 2021-2025 to the most directly comparable measure prepared in accordance with GAAP because P3 is unable to provide this reconciliation without unreasonable effort due to the uncertainty and inherent difficulty of predicting the occurrence, the financial impact, and the periods in which the adjustments may be recognized. For the same reasons, P3 is unable to address the probable significance of the unavailable information, which could be material to future results. ADDITIONAL INFORMATION ABOUT THE PROPOSED BUSINESS COMBINATION AND WHERE TO FIND IT The proposed business combination will be submitted to stockholders of Foresight for their consideration. Foresight filed preliminary a proxy statement (the “Proxy Statement”) with the SEC on August 12, 2021. After the definitive Proxy Statement has been filed, Foresight will mail the definitive Proxy Statement and other relevant documents to its stockholders as of the record date established for voting on the proposed business combination. Foresight's stockholders and other interested persons are advised to read, once available, the preliminary Proxy Statement and any amendments thereto and, once available, the definitive Proxy Statement, in connection with Foresight's solicitation of proxies for its special meeting of stockholders to be held to approve, among other things, the proposed business combination, because these documents will contain important information about Foresight, P3 and the proposed business combination. Investors and securities holders may also obtain a copy of the preliminary or definitive Proxy Statement, once available, as well as other documents filed with the SEC regarding the proposed business combination and other documents filed with the SEC by Foresight, without charge, at the SEC's website located at www.sec.gov or by directing a request to Gateway Investor Relations, (949) 574-3860, FORE@gatewayir.com. INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED OR DISAPPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE. 2

Disclaimer PARTICIPANTS IN THE SOLICITATION Foresight, P3 and certain of their respective directors, executive officers and other members of management and employees may, under SEC rules, be deemed to be participants in the solicitations of proxies from Foresight’s stockholders in connection with the proposed business combination. Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of Foresight’s stockholders in connection with the proposed business combination will be set forth in the Proxy Statement when it is filed with the SEC. You can find more information about Foresight’s directors and executive officers in Foresight’s Annual Report. Additional information regarding the participants in the proxy solicitation and a description of their direct and indirect interests will be included in the Proxy Statement when it becomes available. Stockholders, potential investors and other interested persons should read the Proxy Statement carefully when it becomes available before making any voting or investment decisions. You may obtain free copies of these documents from the sources indicated above. NO OFFER OR SOLICITATION This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. TRADEMARKS This presentation contains trademarks, service marks, trade names and copyrights of P3, Foresight and other companies, which are the property of their respective owners. 3

Foresight Acquisition Corp. Adds Significant Value to P3 Health Partners ■ Currently serves as President and Founder of his family office, ■ Former Partner and Co-Manager of the William Blair Wasson Enterprise Small Institutional portfolio and Small Cap Growth Fund ■ Former CEO and President of Walgreens from 2009 to 2014. Served Walgreens for 34 years, creating significant financial and ■ Over 30 years of experience working with public companies in shareholder value by initiating transformative mergers and the small cap space investments, leading organizational change, assembling diverse ■ Currently the Chairman of the Board of Performance leadership and establishing the company’s position as an Health Systems industry leader ■ Former Partner at Magnetar Capital, LLC, a multi-strategy ■ Invested and nurtured a portfolio of investments by adding value hedge fund through his ability to catalyze relationships for businesses, channel partners, key hires, and strategic investors to build■ Co-founded Cityview Associates, a real estate investment firm sustainable, high-growth businesses that do well by doing good Greg Wasson Michael Balkin ■ Recognized throughout the drugstore and healthcare industry for Chairman of the Board Chief Executive Officer and Director transformational leadership, innovation, bold business decisions, and executing on strategic long-term visions ■ Lifelong leader in the healthcare space and known for his ability■ A pharmacy, health and wellness expert who has led to transform companies and achieve financial and operational transformational change and cost-saving programs in highly success competitive consumer-focused businesses ■ Transformed a small pharmacy benefit management company■ Previously served as an Operating Partner, Advisor and (PBM) called SXC Health Solutions into one of America’s biggest Consultant for Sycamore Partners, specializing in retail and and fastest growing players – then facilitated its $12.8 billion sale consumer investments to Optum ■ Former President and COO of Rite Aid Pharmacy ■ Former CEO of OptumRx from 2015 to 2017 ■ Former CEO and Chairman of Catamaran from 2006 to 2015 Mark Thierer Kermit Crawford Advisor Advisor 4 Deep experience in both private and public markets across Long-term focus on sustainable growth and development Aligned interest across SPAC, Wasson Enterprise and the entirety of the capital structure with the ability to add value investorsForesight Acquisition Corp. Adds Significant Value to P3 Health Partners ■ Currently serves as President and Founder of his family office, ■ Former Partner and Co-Manager of the William Blair Wasson Enterprise Small Institutional portfolio and Small Cap Growth Fund ■ Former CEO and President of Walgreens from 2009 to 2014. Served Walgreens for 34 years, creating significant financial and ■ Over 30 years of experience working with public companies in shareholder value by initiating transformative mergers and the small cap space investments, leading organizational change, assembling diverse ■ Currently the Chairman of the Board of Performance leadership and establishing the company’s position as an Health Systems industry leader ■ Former Partner at Magnetar Capital, LLC, a multi-strategy ■ Invested and nurtured a portfolio of investments by adding value hedge fund through his ability to catalyze relationships for businesses, channel partners, key hires, and strategic investors to build■ Co-founded Cityview Associates, a real estate investment firm sustainable, high-growth businesses that do well by doing good Greg Wasson Michael Balkin ■ Recognized throughout the drugstore and healthcare industry for Chairman of the Board Chief Executive Officer and Director transformational leadership, innovation, bold business decisions, and executing on strategic long-term visions ■ Lifelong leader in the healthcare space and known for his ability■ A pharmacy, health and wellness expert who has led to transform companies and achieve financial and operational transformational change and cost-saving programs in highly success competitive consumer-focused businesses ■ Transformed a small pharmacy benefit management company■ Previously served as an Operating Partner, Advisor and (PBM) called SXC Health Solutions into one of America’s biggest Consultant for Sycamore Partners, specializing in retail and and fastest growing players – then facilitated its $12.8 billion sale consumer investments to Optum ■ Former President and COO of Rite Aid Pharmacy ■ Former CEO of OptumRx from 2015 to 2017 ■ Former CEO and Chairman of Catamaran from 2006 to 2015 Mark Thierer Kermit Crawford Advisor Advisor 4 Deep experience in both private and public markets across Long-term focus on sustainable growth and development Aligned interest across SPAC, Wasson Enterprise and the entirety of the capital structure with the ability to add value investors

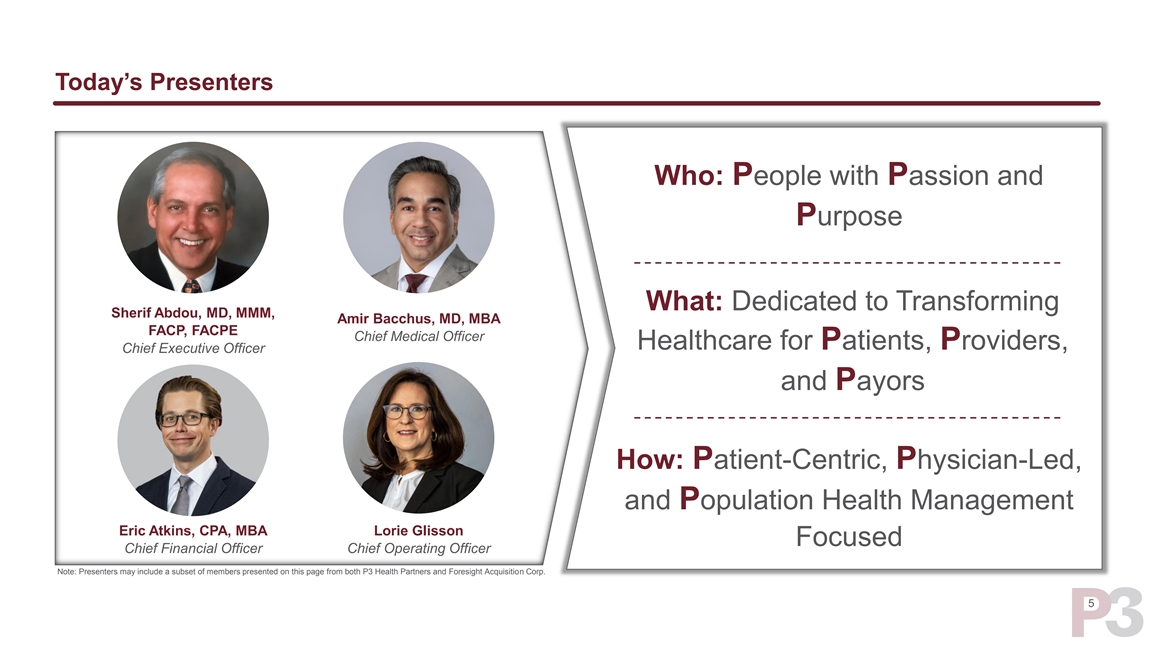

Today’s Presenters Who: People with Passion and Purpose What: Dedicated to Transforming Sherif Abdou, MD, MMM, Amir Bacchus, MD, MBA FACP, FACPE Chief Medical Officer Healthcare for Patients, Providers, Chief Executive Officer and Payors How: Patient-Centric, Physician-Led, and Population Health Management Eric Atkins, CPA, MBA Lorie Glisson Focused Chief Financial Officer Chief Operating Officer Note: Presenters may include a subset of members presented on this page from both P3 Health Partners and Foresight Acquisition Corp. 5Today’s Presenters Who: People with Passion and Purpose What: Dedicated to Transforming Sherif Abdou, MD, MMM, Amir Bacchus, MD, MBA FACP, FACPE Chief Medical Officer Healthcare for Patients, Providers, Chief Executive Officer and Payors How: Patient-Centric, Physician-Led, and Population Health Management Eric Atkins, CPA, MBA Lorie Glisson Focused Chief Financial Officer Chief Operating Officer Note: Presenters may include a subset of members presented on this page from both P3 Health Partners and Foresight Acquisition Corp. 5

OverviewOverview

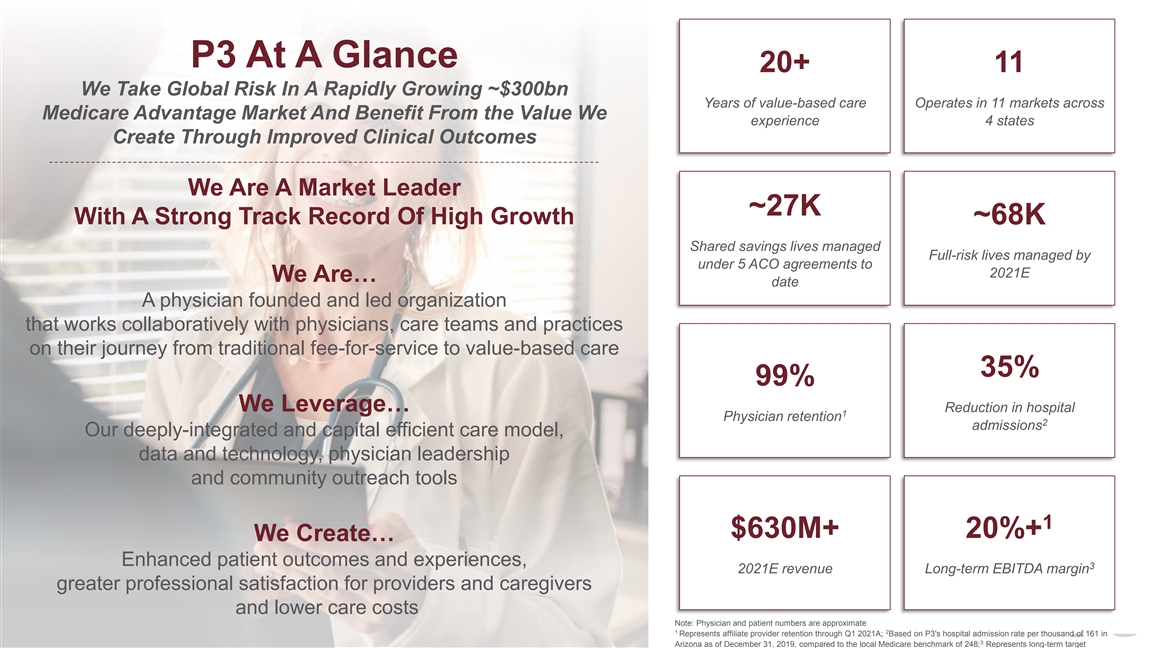

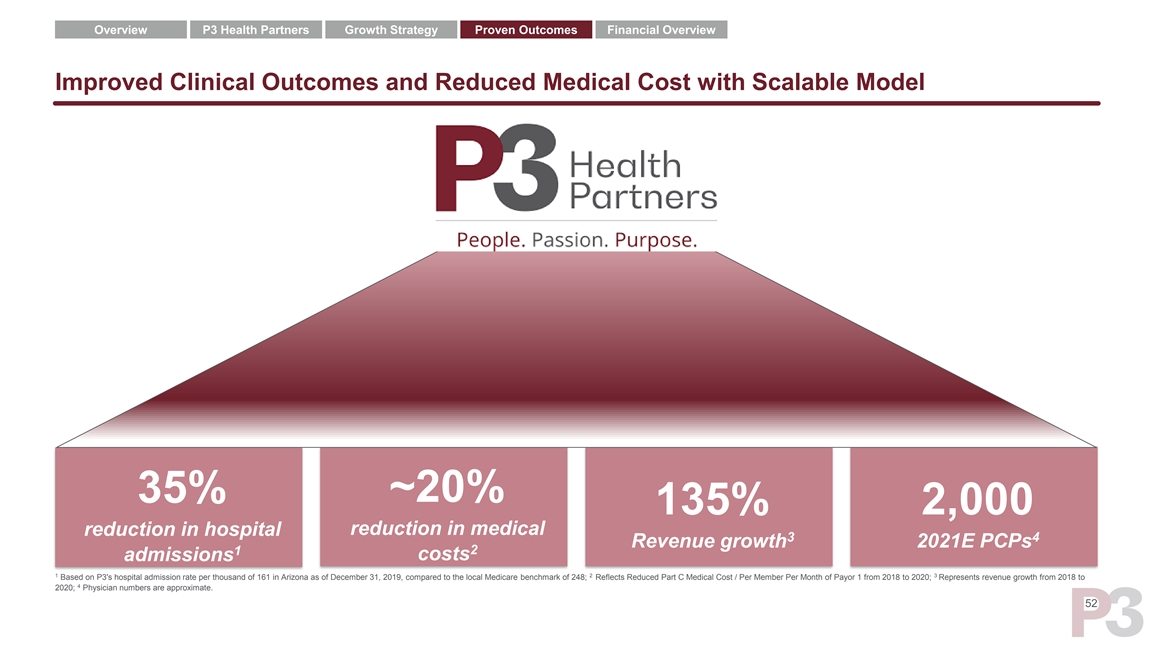

P3 At A Glance 20+ 11 We Take Global Risk In A Rapidly Growing ~$300bn Years of value-based care Operates in 11 markets across Medicare Advantage Market And Benefit From the Value We experience 4 states Create Through Improved Clinical Outcomes We Are A Market Leader ~27K With A Strong Track Record Of High Growth ~68K Shared savings lives managed Full-risk lives managed by under 5 ACO agreements to 2021E We Are… date A physician founded and led organization that works collaboratively with physicians, care teams and practices on their journey from traditional fee-for-service to value-based care 35% 99% We Leverage… Reduction in hospital 1 Physician retention 2 admissions Our deeply-integrated and capital efficient care model, data and technology, physician leadership and community outreach tools 1 $630M+ 20%+ We Create… Enhanced patient outcomes and experiences, 3 2021E revenue Long-term EBITDA margin greater professional satisfaction for providers and caregivers 7 and lower care costs Note: Physician and patient numbers are approximate 1 2 Represents affiliate provider retention through Q1 2021A; Based on P3's hospital admission rate per thousand of 161 in 3 Arizona as of December 31, 2019, compared to the local Medicare benchmark of 248; Represents long-term targetP3 At A Glance 20+ 11 We Take Global Risk In A Rapidly Growing ~$300bn Years of value-based care Operates in 11 markets across Medicare Advantage Market And Benefit From the Value We experience 4 states Create Through Improved Clinical Outcomes We Are A Market Leader ~27K With A Strong Track Record Of High Growth ~68K Shared savings lives managed Full-risk lives managed by under 5 ACO agreements to 2021E We Are… date A physician founded and led organization that works collaboratively with physicians, care teams and practices on their journey from traditional fee-for-service to value-based care 35% 99% We Leverage… Reduction in hospital 1 Physician retention 2 admissions Our deeply-integrated and capital efficient care model, data and technology, physician leadership and community outreach tools 1 $630M+ 20%+ We Create… Enhanced patient outcomes and experiences, 3 2021E revenue Long-term EBITDA margin greater professional satisfaction for providers and caregivers 7 and lower care costs Note: Physician and patient numbers are approximate 1 2 Represents affiliate provider retention through Q1 2021A; Based on P3's hospital admission rate per thousand of 161 in 3 Arizona as of December 31, 2019, compared to the local Medicare benchmark of 248; Represents long-term target

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Vision & Mission Vision Mission To build the greatest population health To be the best health partner for… management company. Patients, Providers & Payors. 8Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Vision & Mission Vision Mission To build the greatest population health To be the best health partner for… management company. Patients, Providers & Payors. 8

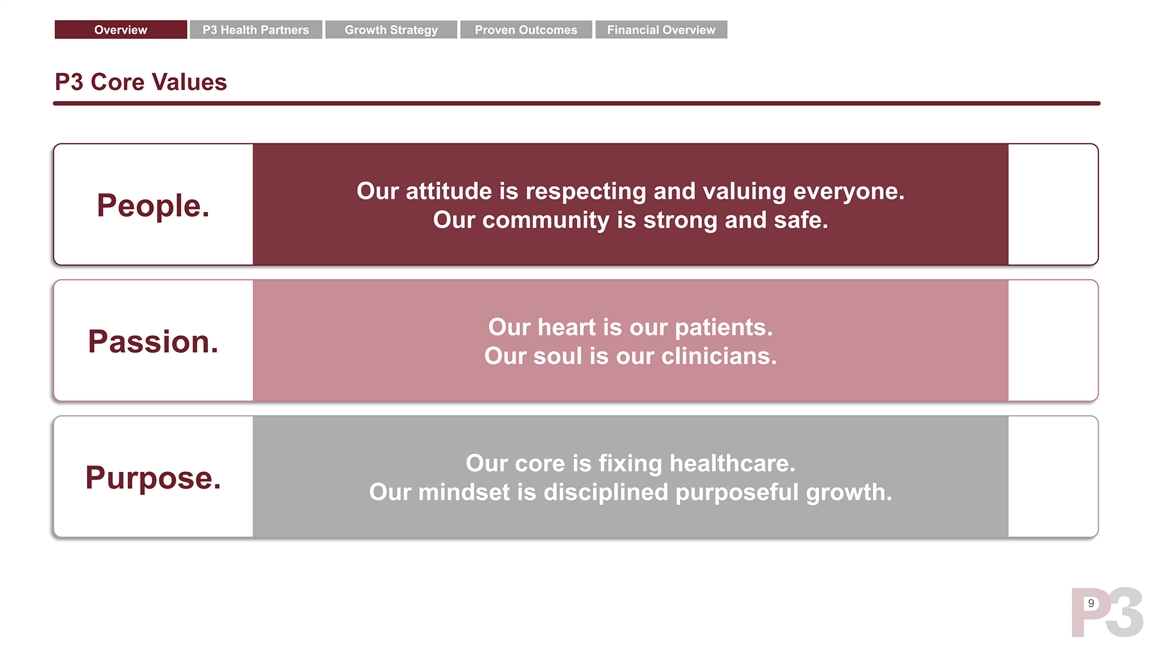

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Core Values Our attitude is respecting and valuing everyone. People. Our community is strong and safe. Our heart is our patients. Passion. Our soul is our clinicians. Our core is fixing healthcare. Purpose. Our mindset is disciplined purposeful growth. 9

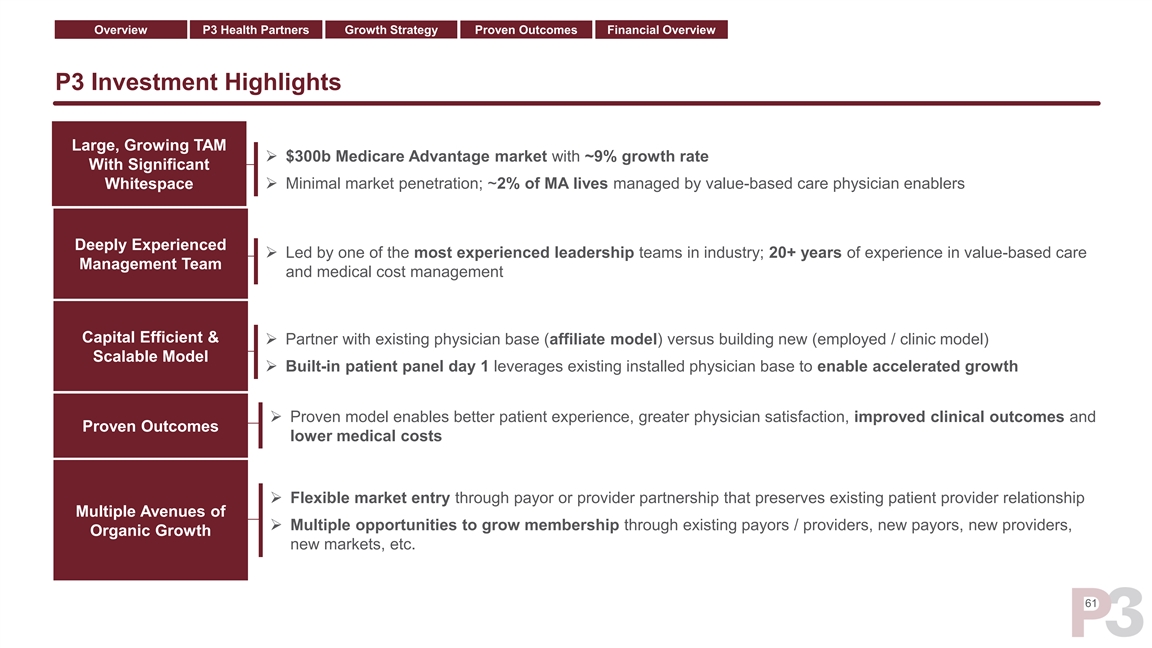

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Investment Highlights Large, Growing TAM With Significant Whitespace Deeply Experienced Management Team Capital Efficient & Scalable Model Proven Outcomes Multiple Avenues of Organic Growth 10Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Investment Highlights Large, Growing TAM With Significant Whitespace Deeply Experienced Management Team Capital Efficient & Scalable Model Proven Outcomes Multiple Avenues of Organic Growth 10

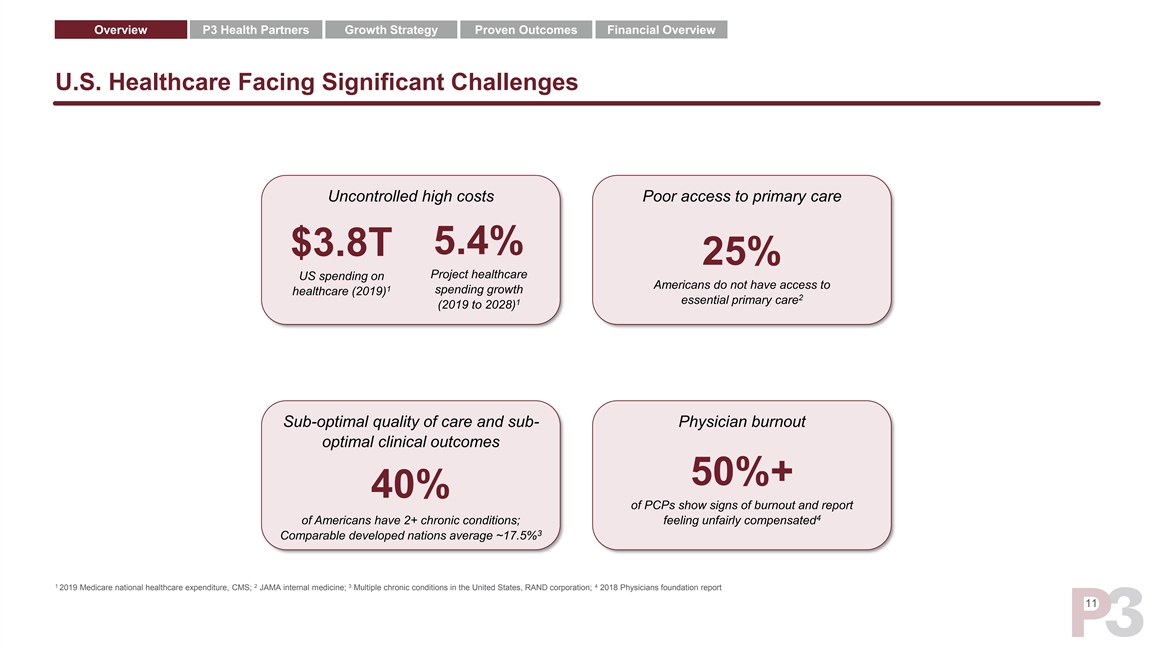

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview U.S. Healthcare Facing Significant Challenges Uncontrolled high costs Poor access to primary care 5.4% $3.8T 25% Project healthcare US spending on Americans do not have access to 1 spending growth healthcare (2019) 2 essential primary care 1 (2019 to 2028) Sub-optimal quality of care and sub- Physician burnout optimal clinical outcomes 50%+ 40% of PCPs show signs of burnout and report 4 of Americans have 2+ chronic conditions; feeling unfairly compensated 3 Comparable developed nations average ~17.5% 1 2 3 4 2019 Medicare national healthcare expenditure, CMS; JAMA internal medicine; Multiple chronic conditions in the United States, RAND corporation; 2018 Physicians foundation report 11Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview U.S. Healthcare Facing Significant Challenges Uncontrolled high costs Poor access to primary care 5.4% $3.8T 25% Project healthcare US spending on Americans do not have access to 1 spending growth healthcare (2019) 2 essential primary care 1 (2019 to 2028) Sub-optimal quality of care and sub- Physician burnout optimal clinical outcomes 50%+ 40% of PCPs show signs of burnout and report 4 of Americans have 2+ chronic conditions; feeling unfairly compensated 3 Comparable developed nations average ~17.5% 1 2 3 4 2019 Medicare national healthcare expenditure, CMS; JAMA internal medicine; Multiple chronic conditions in the United States, RAND corporation; 2018 Physicians foundation report 11

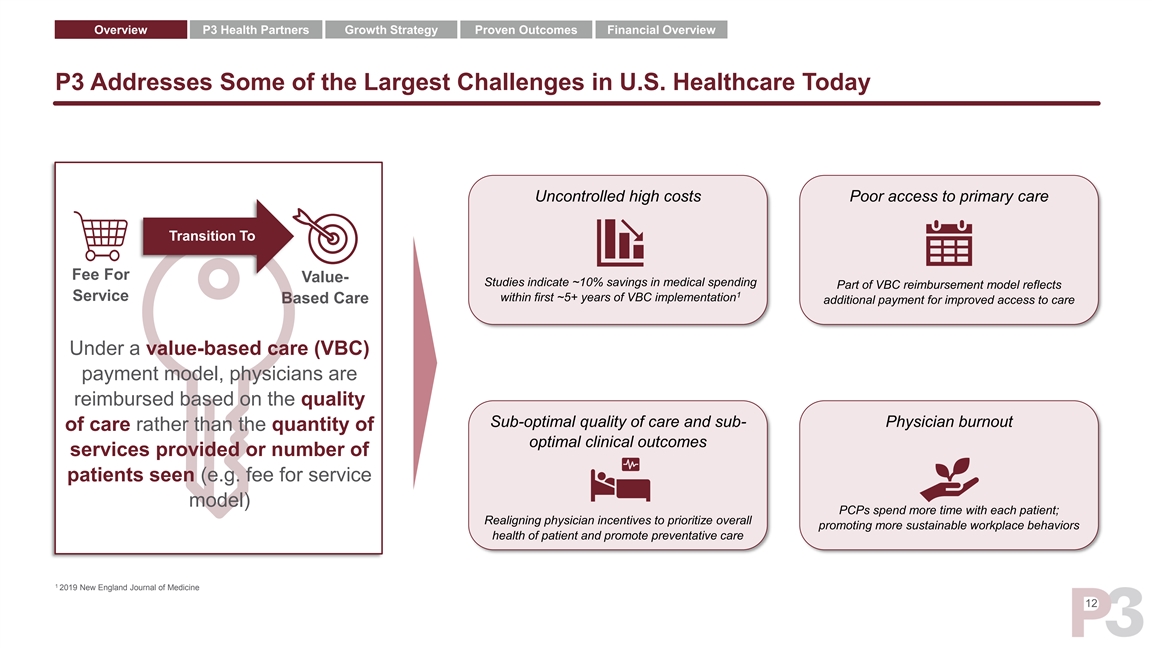

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Addresses Some of the Largest Challenges in U.S. Healthcare Today Uncontrolled high costs Poor access to primary care Transition To X X Fee For Value- Studies indicate ~10% savings in medical spending Part of VBC reimbursement model reflects 1 Service within first ~5+ years of VBC implementation Based Care additional payment for improved access to care Under a value-based care (VBC) payment model, physicians are reimbursed based on the quality Sub-optimal quality of care and sub- Physician burnout of care rather than the quantity of optimal clinical outcomes services provided or number of X patients seen (e.g. fee for service X model) PCPs spend more time with each patient; Realigning physician incentives to prioritize overall promoting more sustainable workplace behaviors health of patient and promote preventative care 1 2019 New England Journal of Medicine 12Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Addresses Some of the Largest Challenges in U.S. Healthcare Today Uncontrolled high costs Poor access to primary care Transition To X X Fee For Value- Studies indicate ~10% savings in medical spending Part of VBC reimbursement model reflects 1 Service within first ~5+ years of VBC implementation Based Care additional payment for improved access to care Under a value-based care (VBC) payment model, physicians are reimbursed based on the quality Sub-optimal quality of care and sub- Physician burnout of care rather than the quantity of optimal clinical outcomes services provided or number of X patients seen (e.g. fee for service X model) PCPs spend more time with each patient; Realigning physician incentives to prioritize overall promoting more sustainable workplace behaviors health of patient and promote preventative care 1 2019 New England Journal of Medicine 12

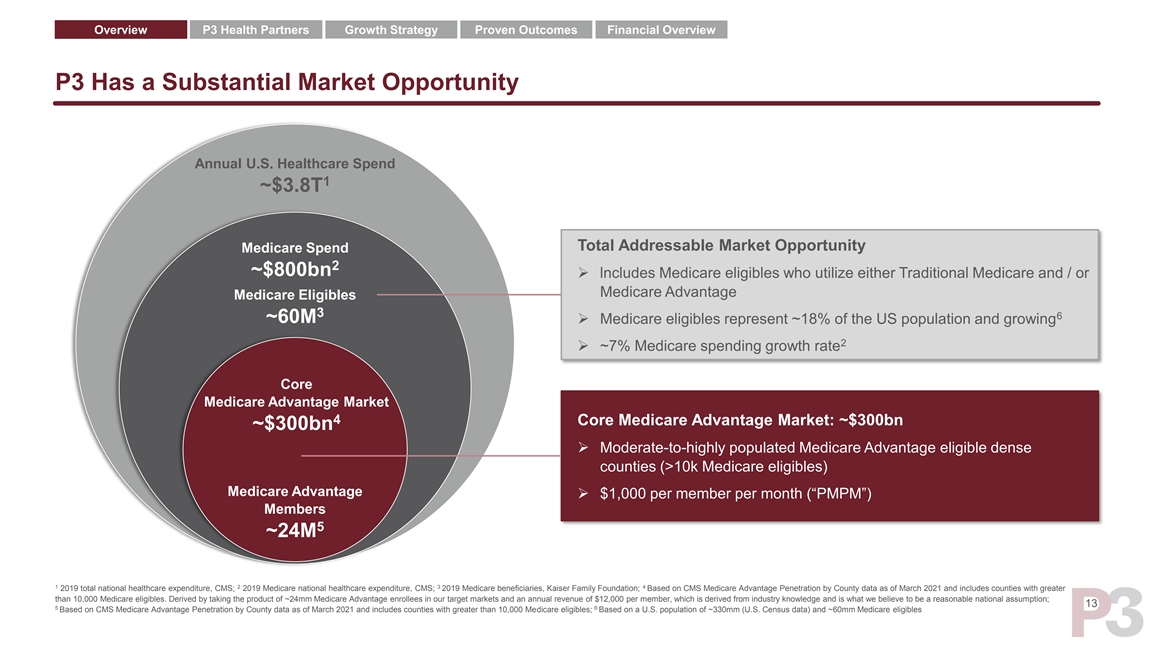

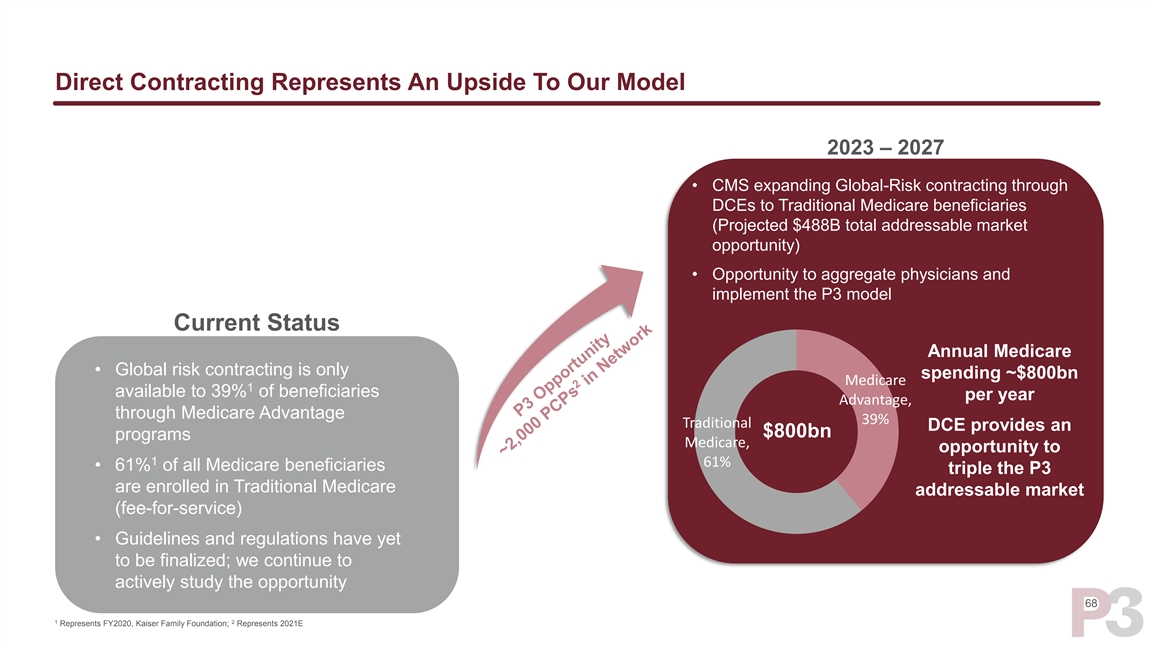

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Has a Substantial Market Opportunity Annual U.S. Healthcare Spend 1 ~$3.8T Total Addressable Market Opportunity Medicare Spend 2 ~$800bn ➢ lncludes Medicare eligibles who utilize either Traditional Medicare and / or Medicare Advantage Medicare Eligibles 3 6 ~60M ➢ Medicare eligibles represent ~18% of the US population and growing 2 ➢ ~7% Medicare spending growth rate Core Medicare Advantage Market 4 Core Medicare Advantage Market: ~$300bn ~$300bn ➢ Moderate-to-highly populated Medicare Advantage eligible dense counties (>10k Medicare eligibles) Medicare Advantage ➢ $1,000 per member per month (“PMPM”) Members 5 ~24M 1 2 3 4 2019 total national healthcare expenditure, CMS; 2019 Medicare national healthcare expenditure, CMS; 2019 Medicare beneficiaries, Kaiser Family Foundation; Based on CMS Medicare Advantage Penetration by County data as of March 2021 and includes counties with greater than 10,000 Medicare eligibles. Derived by taking the product of ~24mm Medicare Advantage enrollees in our target markets and an annual revenue of $12,000 per member, which is derived from industry knowledge and is what we believe to be a reasonable national assumption; 13 5 6 Based on CMS Medicare Advantage Penetration by County data as of March 2021 and includes counties with greater than 10,000 Medicare eligibles; Based on a U.S. population of ~330mm (U.S. Census data) and ~60mm Medicare eligiblesOverview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Has a Substantial Market Opportunity Annual U.S. Healthcare Spend 1 ~$3.8T Total Addressable Market Opportunity Medicare Spend 2 ~$800bn ➢ lncludes Medicare eligibles who utilize either Traditional Medicare and / or Medicare Advantage Medicare Eligibles 3 6 ~60M ➢ Medicare eligibles represent ~18% of the US population and growing 2 ➢ ~7% Medicare spending growth rate Core Medicare Advantage Market 4 Core Medicare Advantage Market: ~$300bn ~$300bn ➢ Moderate-to-highly populated Medicare Advantage eligible dense counties (>10k Medicare eligibles) Medicare Advantage ➢ $1,000 per member per month (“PMPM”) Members 5 ~24M 1 2 3 4 2019 total national healthcare expenditure, CMS; 2019 Medicare national healthcare expenditure, CMS; 2019 Medicare beneficiaries, Kaiser Family Foundation; Based on CMS Medicare Advantage Penetration by County data as of March 2021 and includes counties with greater than 10,000 Medicare eligibles. Derived by taking the product of ~24mm Medicare Advantage enrollees in our target markets and an annual revenue of $12,000 per member, which is derived from industry knowledge and is what we believe to be a reasonable national assumption; 13 5 6 Based on CMS Medicare Advantage Penetration by County data as of March 2021 and includes counties with greater than 10,000 Medicare eligibles; Based on a U.S. population of ~330mm (U.S. Census data) and ~60mm Medicare eligibles

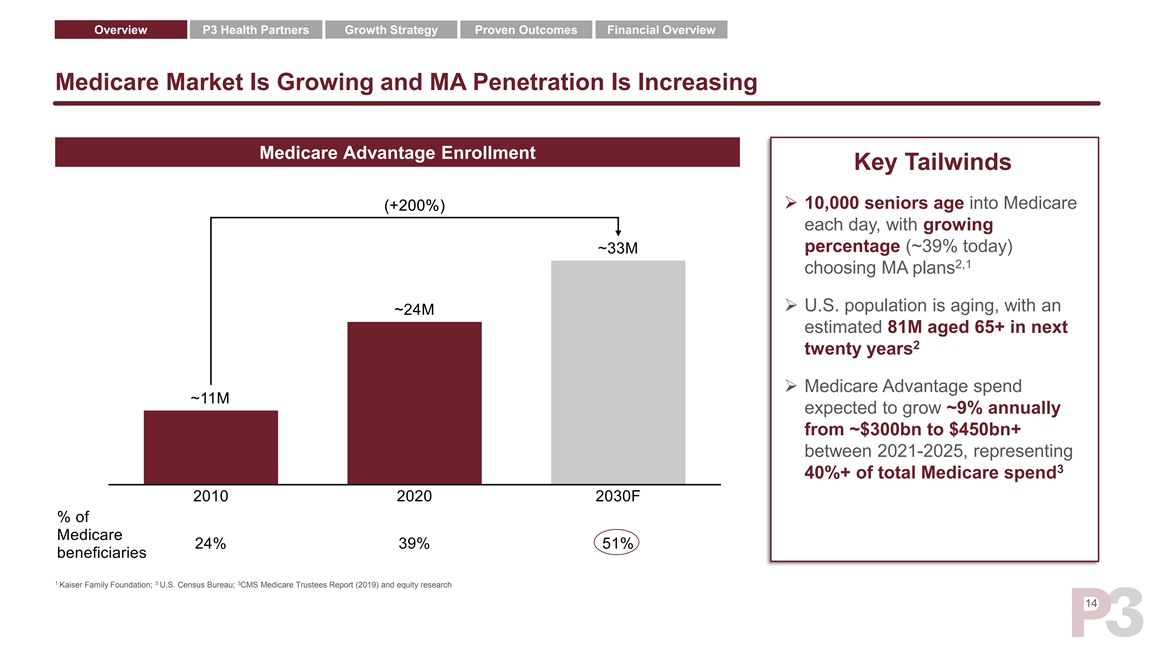

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Medicare Market Is Growing and MA Penetration Is Increasing Medicare Advantage Enrollment Key Tailwinds ➢ 10,000 seniors age into Medicare each day, with growing percentage (~39% today) 2,1 choosing MA plans ➢ U.S. population is aging, with an estimated 81M aged 65+ in next 2 twenty years ➢ Medicare Advantage spend expected to grow ~9% annually from ~$300bn to $450bn+ between 2021-2025, representing 3 40%+ of total Medicare spend 1 3 3 Kaiser Family Foundation; U.S. Census Bureau; CMS Medicare Trustees Report (2019) and equity research 14Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Medicare Market Is Growing and MA Penetration Is Increasing Medicare Advantage Enrollment Key Tailwinds ➢ 10,000 seniors age into Medicare each day, with growing percentage (~39% today) 2,1 choosing MA plans ➢ U.S. population is aging, with an estimated 81M aged 65+ in next 2 twenty years ➢ Medicare Advantage spend expected to grow ~9% annually from ~$300bn to $450bn+ between 2021-2025, representing 3 40%+ of total Medicare spend 1 3 3 Kaiser Family Foundation; U.S. Census Bureau; CMS Medicare Trustees Report (2019) and equity research 14

Market Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Proven Board With Extensive Healthcare Expertise Greg Wasson Mark Thierer Sherif Abdou, MD Amir Bacchus, MD Director Chairman of the Board Chief Executive Officer & Director Chief Medical Officer & Director • CEO & President, Walgreens • CEO, OptumRx• Co-Founder & CEO, HealthCare • Co-Founder & CMO, HealthCare Partners NV Partners NV • CEO & Chairman of Catamaran • Co-Founder & CEO, Pinnacle Health • Co-Founder & CMO, Pinnacle Health System System 30+ Years in Healthcare 30 Years+ in Healthcare 30 Years in Healthcare 23 Years in Healthcare Lawrence B. Leisure Mary Tolan Greg Kazarian Thomas E. Price, MD Jeff Park Director Director Director Director Independent Director rd • Founder & Co-Managing Partner, • Founder & Co-Managing Partner, • Executive Chair & CEO, Recovery • 23 U.S. Secretary, Department of• Chairman & CEO, WellDyneRx Ways Health and Human Services (HHS) Chicago Pacific Founders Chicago Pacific Founders • COO & EVP, Optum • Director, BioIntelliSense• CEO, Founder & Board Chair, R1-• CPO & General Counsel, R1-RCM• Co-Founder, Largest Private Non- Academic Orthopedic Practice in US RCM 30+ Years in Healthcare 18 Years in Healthcare 15 Years in Healthcare 30+ Years in Healthcare 15 Years in Healthcare 15Market Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Proven Board With Extensive Healthcare Expertise Greg Wasson Mark Thierer Sherif Abdou, MD Amir Bacchus, MD Director Chairman of the Board Chief Executive Officer & Director Chief Medical Officer & Director • CEO & President, Walgreens • CEO, OptumRx• Co-Founder & CEO, HealthCare • Co-Founder & CMO, HealthCare Partners NV Partners NV • CEO & Chairman of Catamaran • Co-Founder & CEO, Pinnacle Health • Co-Founder & CMO, Pinnacle Health System System 30+ Years in Healthcare 30 Years+ in Healthcare 30 Years in Healthcare 23 Years in Healthcare Lawrence B. Leisure Mary Tolan Greg Kazarian Thomas E. Price, MD Jeff Park Director Director Director Director Independent Director rd • Founder & Co-Managing Partner, • Founder & Co-Managing Partner, • Executive Chair & CEO, Recovery • 23 U.S. Secretary, Department of• Chairman & CEO, WellDyneRx Ways Health and Human Services (HHS) Chicago Pacific Founders Chicago Pacific Founders • COO & EVP, Optum • Director, BioIntelliSense• CEO, Founder & Board Chair, R1-• CPO & General Counsel, R1-RCM• Co-Founder, Largest Private Non- Academic Orthopedic Practice in US RCM 30+ Years in Healthcare 18 Years in Healthcare 15 Years in Healthcare 30+ Years in Healthcare 15 Years in Healthcare 15

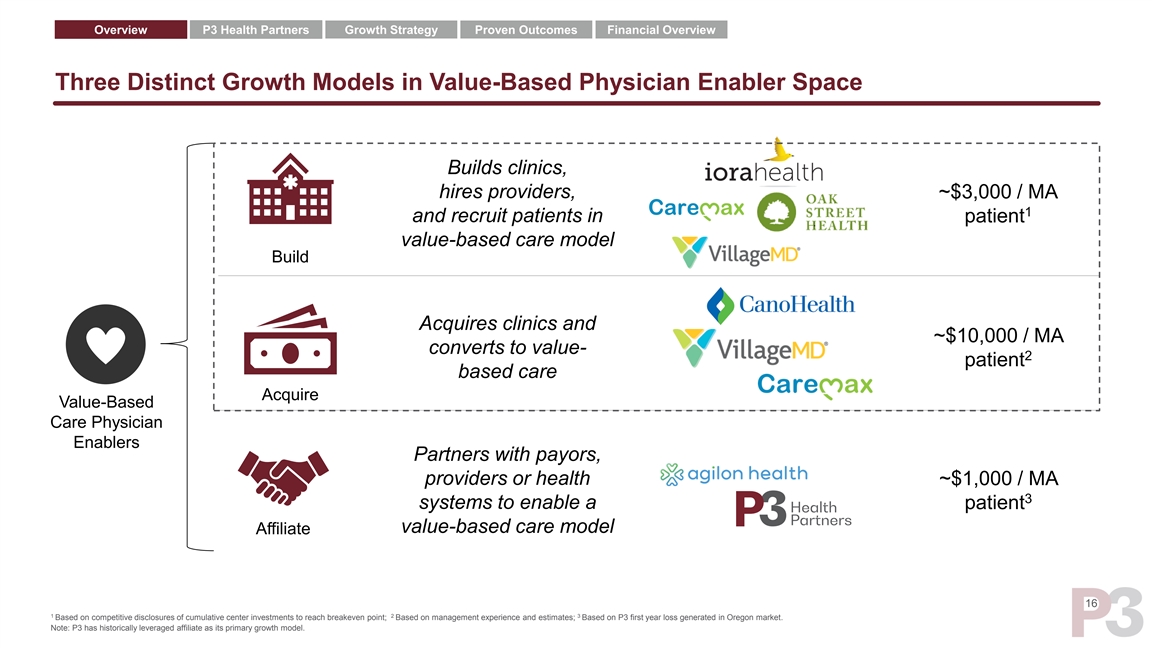

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Three Distinct Growth Models in Value-Based Physician Enabler Space Builds clinics, hires providers, ~$3,000 / MA 1 and recruit patients in patient value-based care model Build Acquires clinics and ~$10,000 / MA converts to value- 2 patient based care Acquire Value-Based Care Physician Enablers Partners with payors, providers or health ~$1,000 / MA 3 systems to enable a patient value-based care model Affiliate 16 1 2 3 Based on competitive disclosures of cumulative center investments to reach breakeven point; Based on management experience and estimates; Based on P3 first year loss generated in Oregon market. Note: P3 has historically leveraged affiliate as its primary growth model.

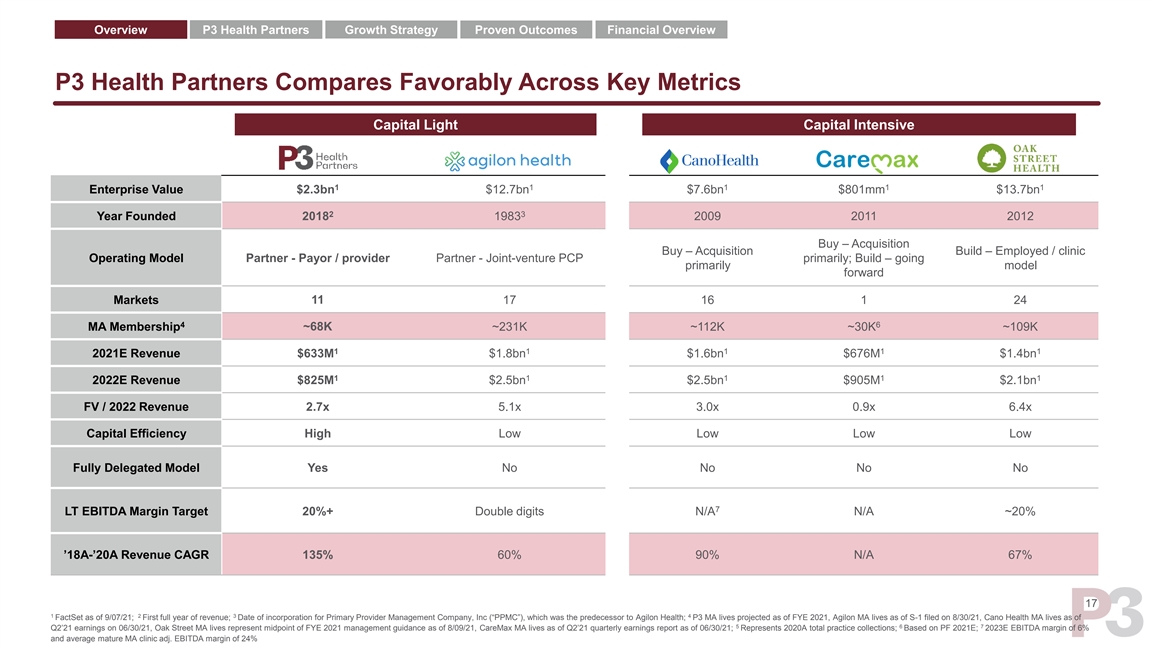

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Health Partners Compares Favorably Across Key Metrics Capital Light Capital Intensive 1 1 1 1 1 Enterprise Value $2.3bn $12.7bn $7.6bn $801mm $13.7bn 2 3 Year Founded 2018 1983 2009 2011 2012 Buy – Acquisition Buy – Acquisition Build – Employed / clinic Operating Model Partner - Payor / provider Partner - Joint-venture PCP primarily; Build – going primarily model forward Markets 11 17 16 1 24 4 6 MA Membership ~68K ~231K ~112K ~30K ~109K 1 1 1 1 1 2021E Revenue $633M $1.8bn $1.6bn $676M $1.4bn 1 1 1 1 1 2022E Revenue $825M $2.5bn $2.5bn $905M $2.1bn FV / 2022 Revenue 2.7x 5.1x 3.0x 0.9x 6.4x Capital Efficiency High Low Low Low Low Fully Delegated Model Yes No No No No 7 LT EBITDA Margin Target 20%+ Double digits N/A N/A ~20% ’18A-’20A Revenue CAGR 135% 60% 90% N/A 67% 17 1 2 3 4 FactSet as of 9/07/21; First full year of revenue; Date of incorporation for Primary Provider Management Company, Inc (“PPMC”), which was the predecessor to Agilon Health; P3 MA lives projected as of FYE 2021, Agilon MA lives as of S-1 filed on 8/30/21, Cano Health MA lives as of 5 6 7 Q2’21 earnings on 06/30/21, Oak Street MA lives represent midpoint of FYE 2021 management guidance as of 8/09/21, CareMax MA lives as of Q2’21 quarterly earnings report as of 06/30/21; Represents 2020A total practice collections; Based on PF 2021E; 2023E EBITDA margin of 6% and average mature MA clinic adj. EBITDA margin of 24%Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Health Partners Compares Favorably Across Key Metrics Capital Light Capital Intensive 1 1 1 1 1 Enterprise Value $2.3bn $12.7bn $7.6bn $801mm $13.7bn 2 3 Year Founded 2018 1983 2009 2011 2012 Buy – Acquisition Buy – Acquisition Build – Employed / clinic Operating Model Partner - Payor / provider Partner - Joint-venture PCP primarily; Build – going primarily model forward Markets 11 17 16 1 24 4 6 MA Membership ~68K ~231K ~112K ~30K ~109K 1 1 1 1 1 2021E Revenue $633M $1.8bn $1.6bn $676M $1.4bn 1 1 1 1 1 2022E Revenue $825M $2.5bn $2.5bn $905M $2.1bn FV / 2022 Revenue 2.7x 5.1x 3.0x 0.9x 6.4x Capital Efficiency High Low Low Low Low Fully Delegated Model Yes No No No No 7 LT EBITDA Margin Target 20%+ Double digits N/A N/A ~20% ’18A-’20A Revenue CAGR 135% 60% 90% N/A 67% 17 1 2 3 4 FactSet as of 9/07/21; First full year of revenue; Date of incorporation for Primary Provider Management Company, Inc (“PPMC”), which was the predecessor to Agilon Health; P3 MA lives projected as of FYE 2021, Agilon MA lives as of S-1 filed on 8/30/21, Cano Health MA lives as of 5 6 7 Q2’21 earnings on 06/30/21, Oak Street MA lives represent midpoint of FYE 2021 management guidance as of 8/09/21, CareMax MA lives as of Q2’21 quarterly earnings report as of 06/30/21; Represents 2020A total practice collections; Based on PF 2021E; 2023E EBITDA margin of 6% and average mature MA clinic adj. EBITDA margin of 24%

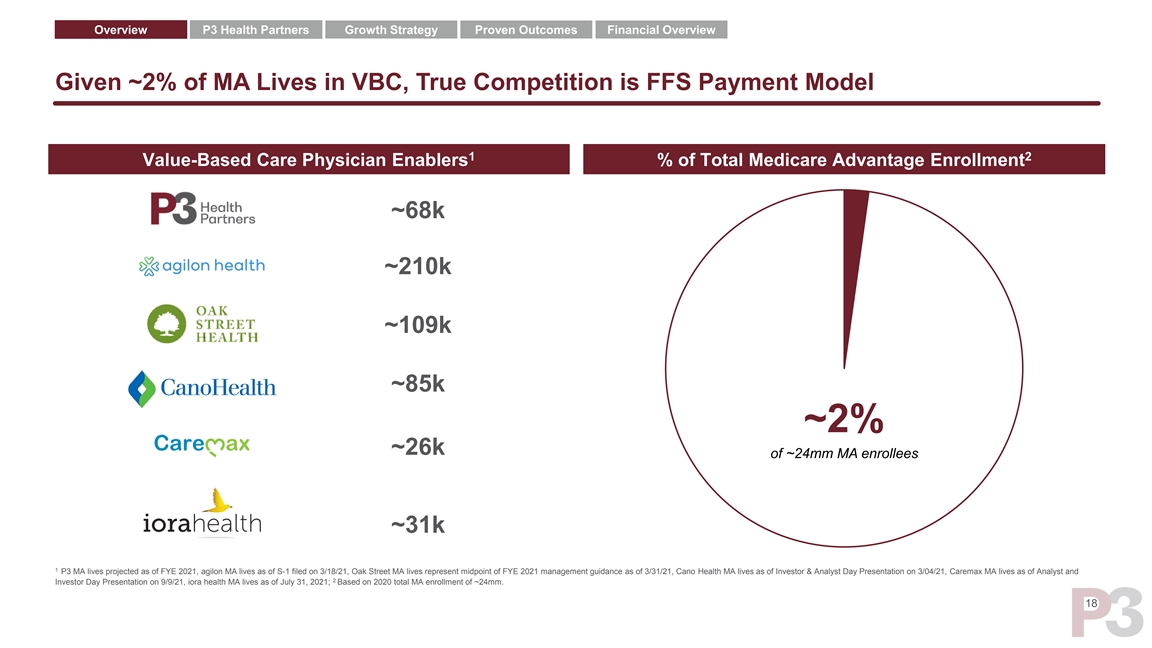

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Given ~2% of MA Lives in VBC, True Competition is FFS Payment Model 1 2 Value-Based Care Physician Enablers % of Total Medicare Advantage Enrollment ~68k ~210k ~109k ~85k ~2% ~26k of ~24mm MA enrollees ~31k 1 P3 MA lives projected as of FYE 2021, agilon MA lives as of S-1 filed on 3/18/21, Oak Street MA lives represent midpoint of FYE 2021 management guidance as of 3/31/21, Cano Health MA lives as of Investor & Analyst Day Presentation on 3/04/21, Caremax MA lives as of Analyst and 2 Investor Day Presentation on 9/9/21, iora health MA lives as of July 31, 2021; Based on 2020 total MA enrollment of ~24mm. 18Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Given ~2% of MA Lives in VBC, True Competition is FFS Payment Model 1 2 Value-Based Care Physician Enablers % of Total Medicare Advantage Enrollment ~68k ~210k ~109k ~85k ~2% ~26k of ~24mm MA enrollees ~31k 1 P3 MA lives projected as of FYE 2021, agilon MA lives as of S-1 filed on 3/18/21, Oak Street MA lives represent midpoint of FYE 2021 management guidance as of 3/31/21, Cano Health MA lives as of Investor & Analyst Day Presentation on 3/04/21, Caremax MA lives as of Analyst and 2 Investor Day Presentation on 9/9/21, iora health MA lives as of July 31, 2021; Based on 2020 total MA enrollment of ~24mm. 18

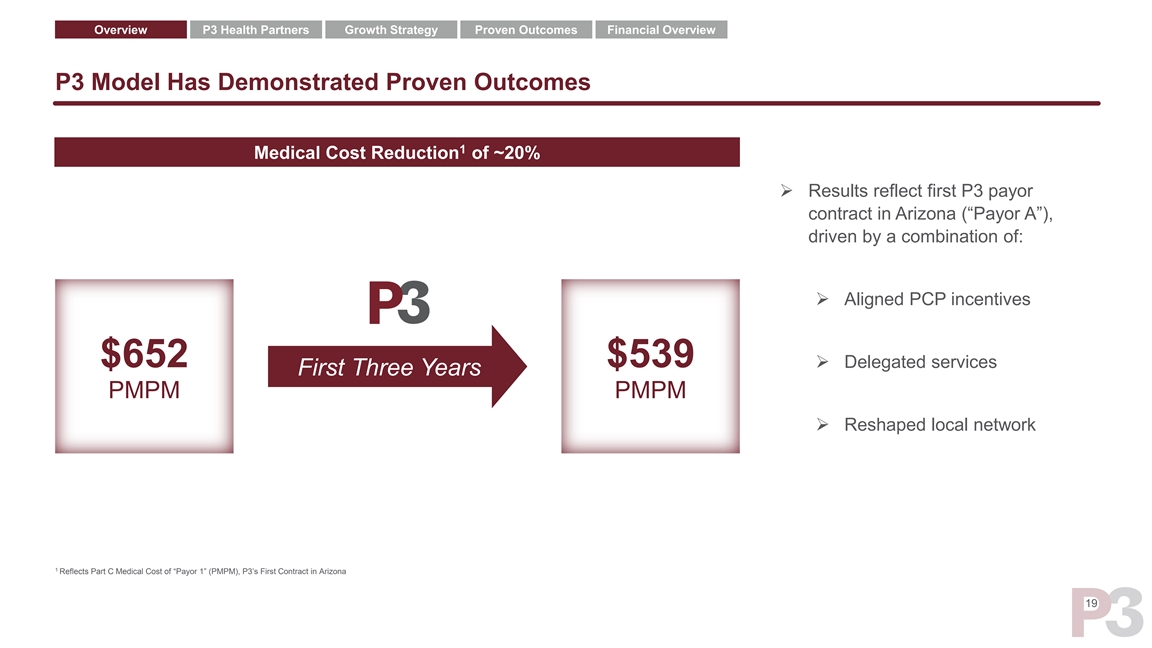

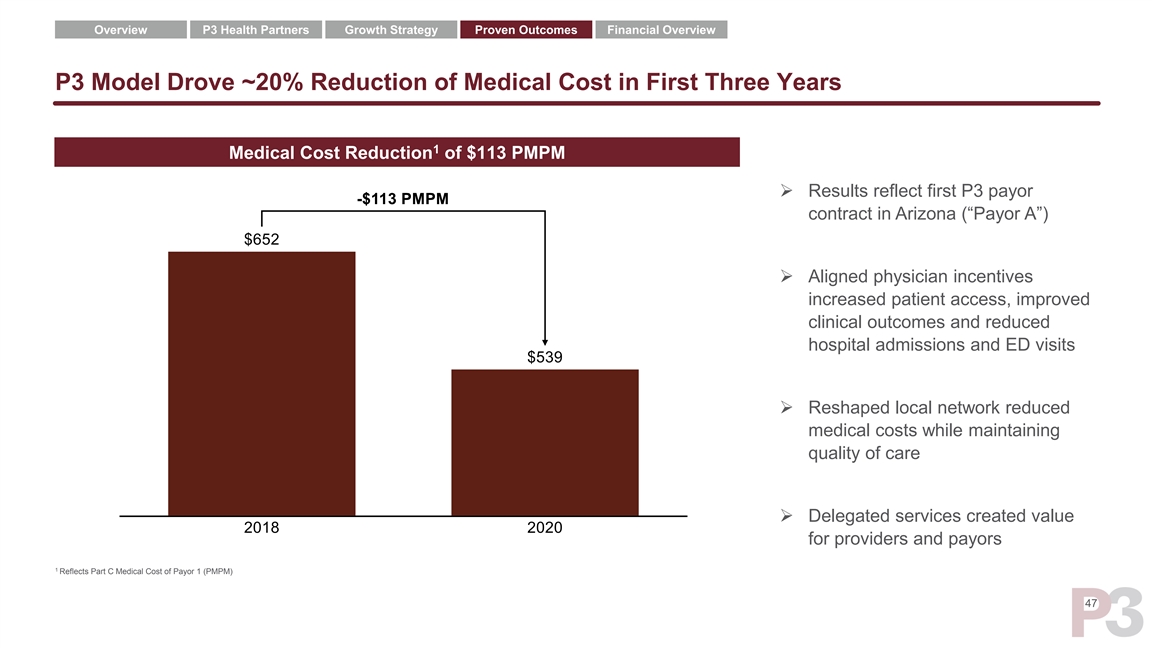

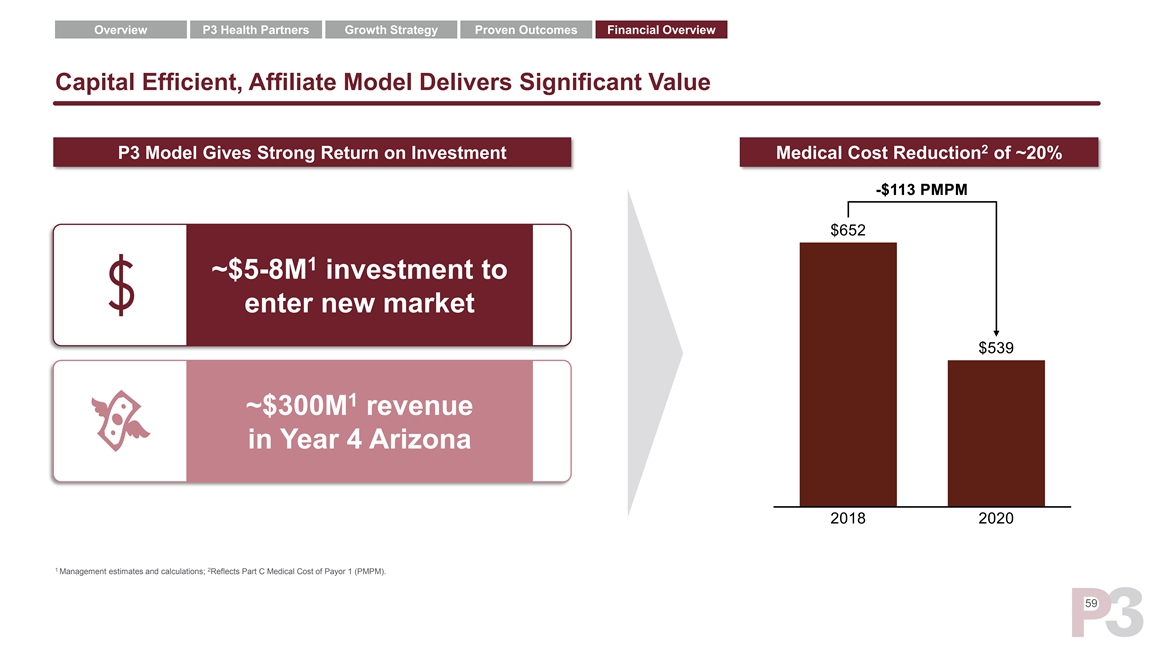

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Model Has Demonstrated Proven Outcomes 1 Medical Cost Reduction of ~20% ➢ Results reflect first P3 payor contract in Arizona (“Payor A”), driven by a combination of: ➢ Aligned PCP incentives $652 $539 ➢ Delegated services First Three Years PMPM PMPM ➢ Reshaped local network 1 Reflects Part C Medical Cost of “Payor 1” (PMPM), P3’s First Contract in Arizona 19Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Model Has Demonstrated Proven Outcomes 1 Medical Cost Reduction of ~20% ➢ Results reflect first P3 payor contract in Arizona (“Payor A”), driven by a combination of: ➢ Aligned PCP incentives $652 $539 ➢ Delegated services First Three Years PMPM PMPM ➢ Reshaped local network 1 Reflects Part C Medical Cost of “Payor 1” (PMPM), P3’s First Contract in Arizona 19

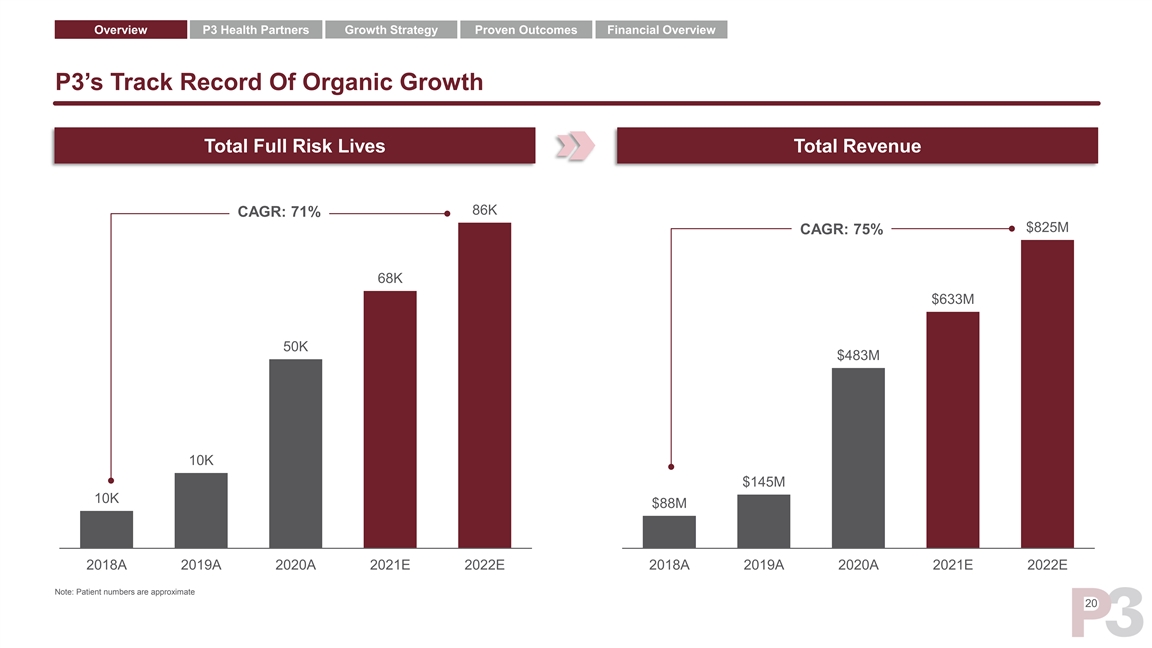

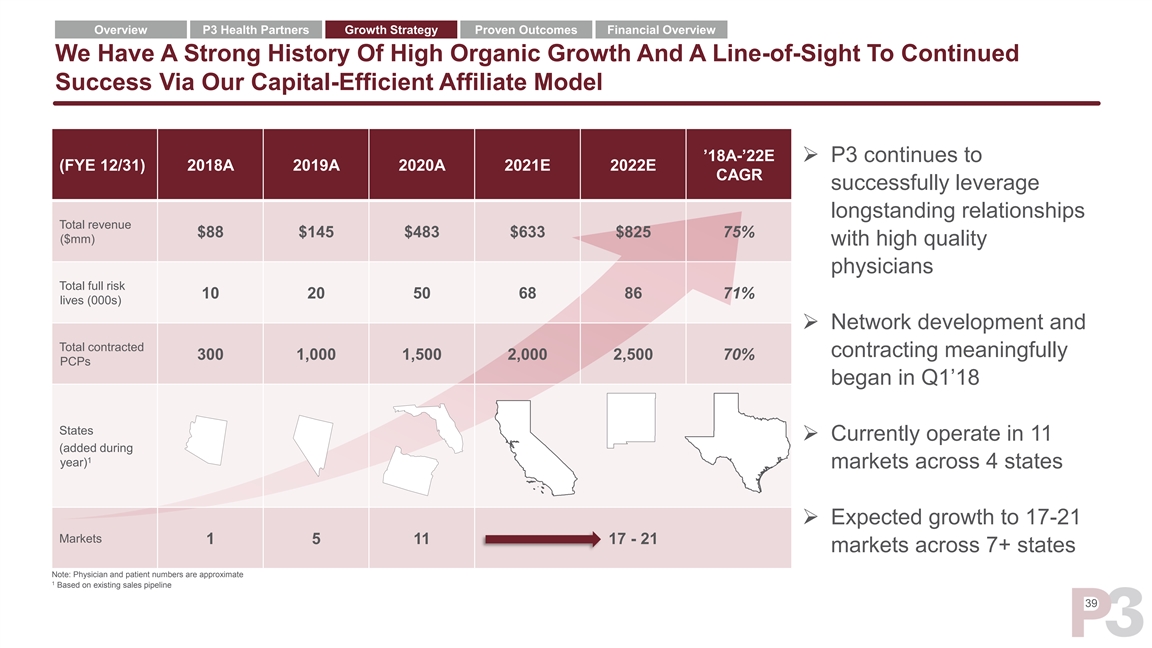

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3’s Track Record Of Organic Growth Total Full Risk Lives Total Revenue 86K CAGR: 71% $825M CAGR: 75% 68K $633M 50K $483M 10K $145M 10K $88M 2018A 2019A 2020A 2021E 2022E 2018A 2019A 2020A 2021E 2022E Note: Patient numbers are approximate 20Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3’s Track Record Of Organic Growth Total Full Risk Lives Total Revenue 86K CAGR: 71% $825M CAGR: 75% 68K $633M 50K $483M 10K $145M 10K $88M 2018A 2019A 2020A 2021E 2022E 2018A 2019A 2020A 2021E 2022E Note: Patient numbers are approximate 20

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Investment Highlights Large, Growing TAM With Significant Whitespace Deeply Experienced Management Team Capital Efficient & Scalable Model Proven Outcomes Multiple Avenues of Organic Growth 21Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Investment Highlights Large, Growing TAM With Significant Whitespace Deeply Experienced Management Team Capital Efficient & Scalable Model Proven Outcomes Multiple Avenues of Organic Growth 21

P3 OverviewP3 Overview

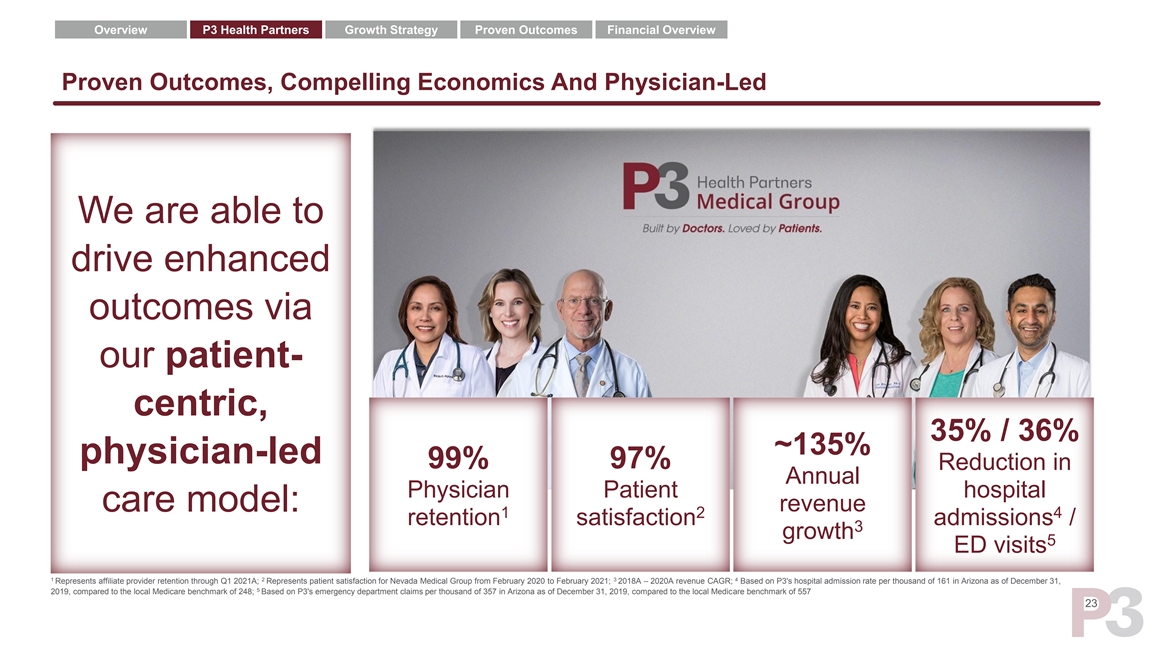

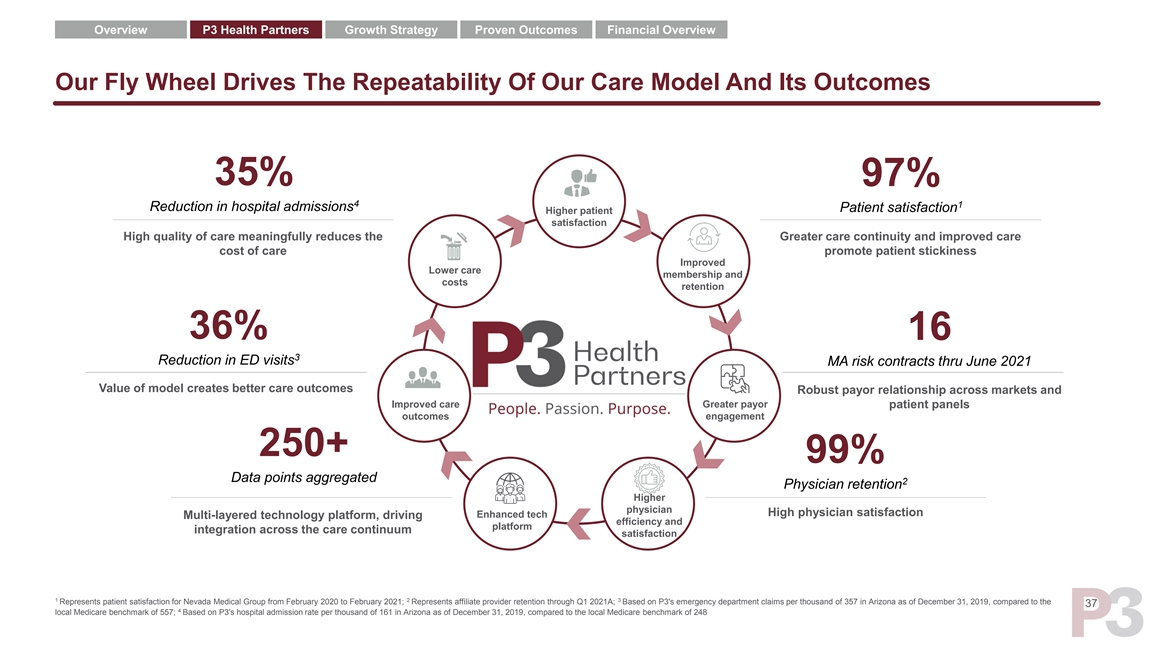

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Proven Outcomes, Compelling Economics And Physician-Led We are able to drive enhanced outcomes via our patient- centric, 35% / 36% ~135% physician-led 99% 97% Reduction in Annual Physician Patient hospital revenue care model: 1 2 4 retention satisfaction admissions / 3 growth 5 ED visits 1 2 3 4 Represents affiliate provider retention through Q1 2021A; Represents patient satisfaction for Nevada Medical Group from February 2020 to February 2021; 2018A – 2020A revenue CAGR; Based on P3's hospital admission rate per thousand of 161 in Arizona as of December 31, 5 2019, compared to the local Medicare benchmark of 248; Based on P3's emergency department claims per thousand of 357 in Arizona as of December 31, 2019, compared to the local Medicare benchmark of 557 23Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Proven Outcomes, Compelling Economics And Physician-Led We are able to drive enhanced outcomes via our patient- centric, 35% / 36% ~135% physician-led 99% 97% Reduction in Annual Physician Patient hospital revenue care model: 1 2 4 retention satisfaction admissions / 3 growth 5 ED visits 1 2 3 4 Represents affiliate provider retention through Q1 2021A; Represents patient satisfaction for Nevada Medical Group from February 2020 to February 2021; 2018A – 2020A revenue CAGR; Based on P3's hospital admission rate per thousand of 161 in Arizona as of December 31, 5 2019, compared to the local Medicare benchmark of 248; Based on P3's emergency department claims per thousand of 357 in Arizona as of December 31, 2019, compared to the local Medicare benchmark of 557 23

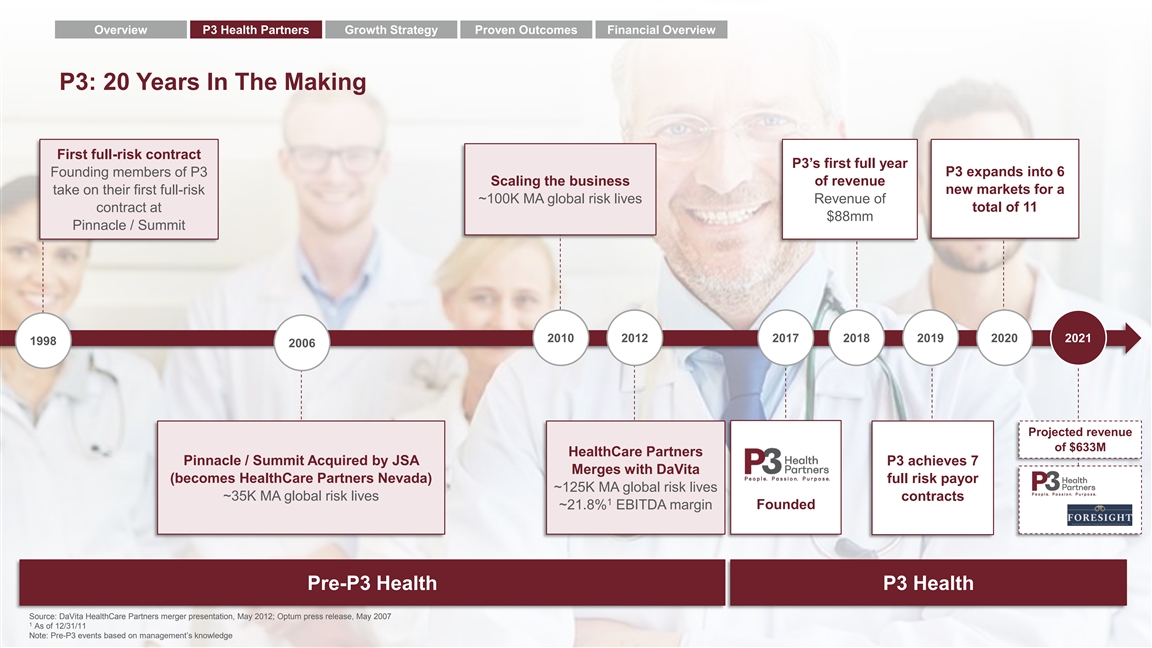

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3: 20 Years In The Making First full-risk contract P3’s first full year P3 expands into 6 Founding members of P3 Scaling the business of revenue new markets for a take on their first full-risk ~100K MA global risk lives Revenue of contract at total of 11 $88mm Pinnacle / Summit 2010 2012 2017 2018 2019 2020 2021 1998 2006 Projected revenue of $633M HealthCare Partners Pinnacle / Summit Acquired by JSA P3 achieves 7 Merges with DaVita (becomes HealthCare Partners Nevada) full risk payor ~125K MA global risk lives ~35K MA global risk lives contracts 1 ~21.8% EBITDA margin Founded Pre-P3 Health P3 Health 24 Source: DaVita HealthCare Partners merger presentation, May 2012; Optum press release, May 2007 1 As of 12/31/11 Note: Pre-P3 events based on management’s knowledgeOverview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3: 20 Years In The Making First full-risk contract P3’s first full year P3 expands into 6 Founding members of P3 Scaling the business of revenue new markets for a take on their first full-risk ~100K MA global risk lives Revenue of contract at total of 11 $88mm Pinnacle / Summit 2010 2012 2017 2018 2019 2020 2021 1998 2006 Projected revenue of $633M HealthCare Partners Pinnacle / Summit Acquired by JSA P3 achieves 7 Merges with DaVita (becomes HealthCare Partners Nevada) full risk payor ~125K MA global risk lives ~35K MA global risk lives contracts 1 ~21.8% EBITDA margin Founded Pre-P3 Health P3 Health 24 Source: DaVita HealthCare Partners merger presentation, May 2012; Optum press release, May 2007 1 As of 12/31/11 Note: Pre-P3 events based on management’s knowledge

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Physician-Led, Deeply Experienced Management Team With 20 Years+ In Value-Based Care Sherif Abdou, MD, Amir Bacchus, MD, MBA Lorie Glisson Todd Lefkowitz, MHA MMM, FACP, FACPE Chief Executive Officer Chief Medical Officer Chief Operating Officer Chief Managed Care Officer • Co-Founder & CEO, HealthCare • Co-Founder & CMO, HealthCare • President & CEO, HealthCare • SVP, Managed Care Operations & Partners Nevada Partners Nevada Partners Florida Network Development, HealthCare Partners • Co-Founder & CEO, Pinnacle Health • Co-Founder & CMO, Pinnacle Health • President & CEO, JSA Healthcare System System Corporation • VP, Network, PacifiCare & UnitedHealthcare-Nevada 30 Years of Experience 25 Years of Experience 25 Years of Experience 20 Years of Experience Sarah Bussmann, Scott Keim Jessica Puathasnanon, JD, LLM Eric Atkins, CPA, MBA BSN-RN, CRNI, MHA Chief Growth Officer EVP, Population Health Chief Legal Officer Chief Financial Officer Management • Executive Director of Business • Chief Counsel & Compliance Officer, • CFO, Sprout Pharmaceuticals Medtronic Diabetes Development, Aetna• Associate VP, Clinical Quality, • Divisional CFO, Hillrom DaVita HealthCare Partners • Senior Vice President, Contracting • Director, KPMG • Director, KPMG and Strategy, Bravo Health • SEC Enforcement 30 Years of Experience 10 Years of Experience 11 Years in Healthcare 9 Years in Healthcare 25

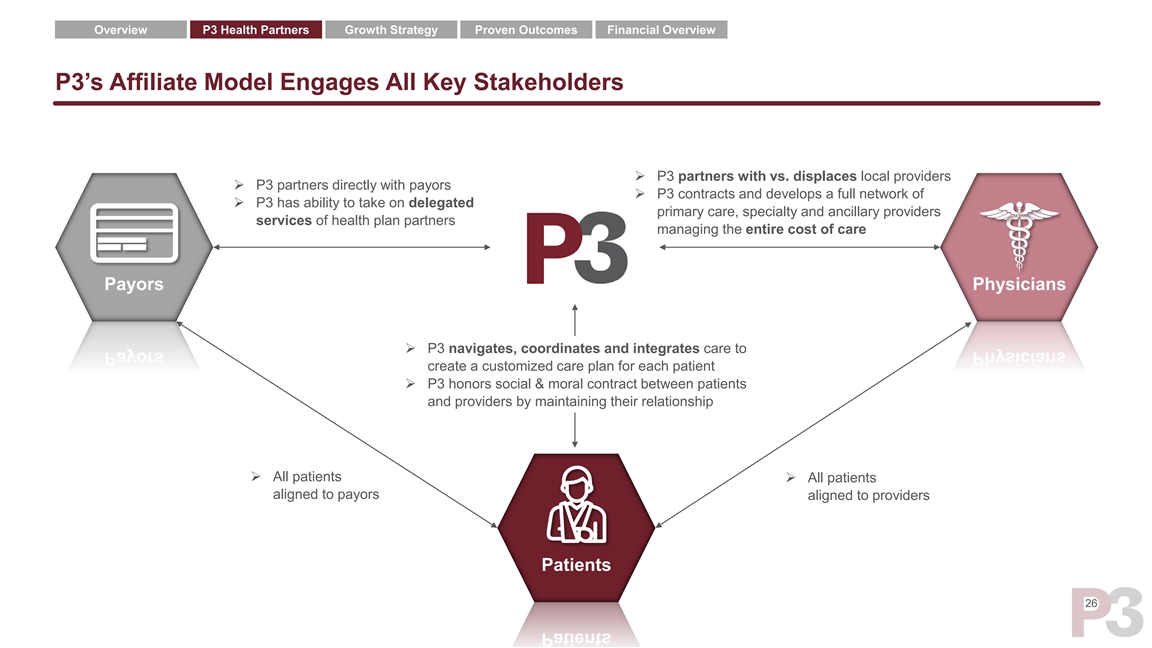

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3’s Affiliate Model Engages All Key Stakeholders ➢ P3 partners with vs. displaces local providers ➢ P3 partners directly with payors ➢ P3 contracts and develops a full network of ➢ P3 has ability to take on delegated primary care, specialty and ancillary providers services of health plan partners managing the entire cost of care Payors Physicians ➢ P3 navigates, coordinates and integrates care to create a customized care plan for each patient ➢ P3 honors social & moral contract between patients and providers by maintaining their relationship ➢ All patients ➢ All patients aligned to payors aligned to providers Patients 26Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3’s Affiliate Model Engages All Key Stakeholders ➢ P3 partners with vs. displaces local providers ➢ P3 partners directly with payors ➢ P3 contracts and develops a full network of ➢ P3 has ability to take on delegated primary care, specialty and ancillary providers services of health plan partners managing the entire cost of care Payors Physicians ➢ P3 navigates, coordinates and integrates care to create a customized care plan for each patient ➢ P3 honors social & moral contract between patients and providers by maintaining their relationship ➢ All patients ➢ All patients aligned to payors aligned to providers Patients 26

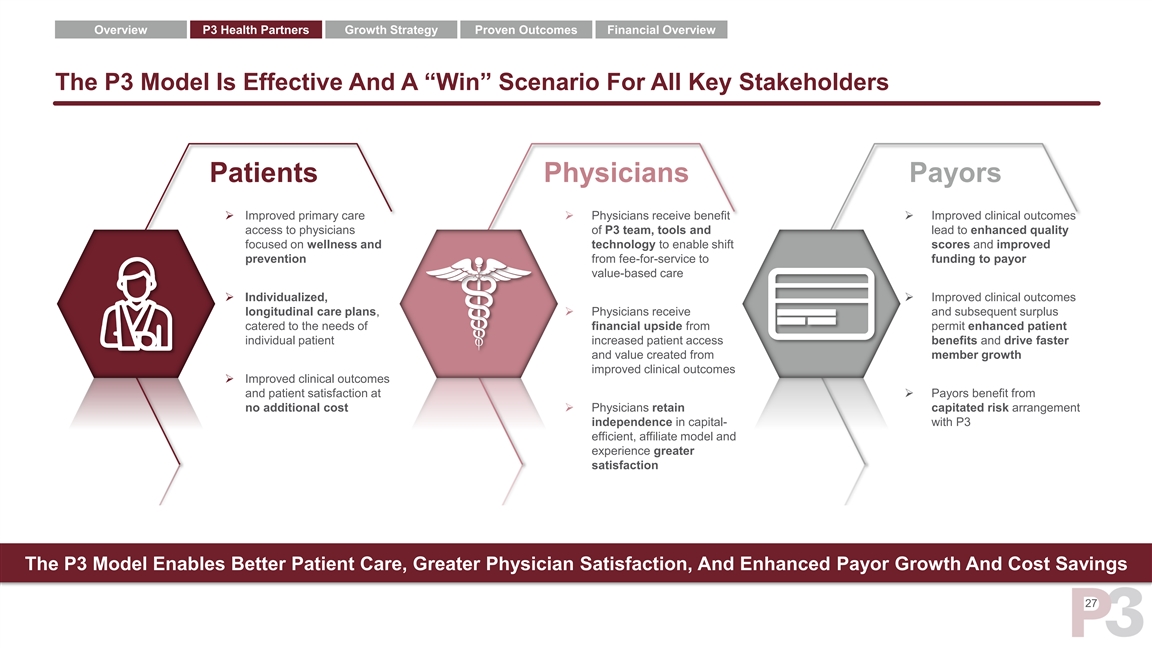

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview The P3 Model Is Effective And A “Win” Scenario For All Key Stakeholders Patients Physicians Payors ➢ Improved primary care ➢ Physicians receive benefit ➢ Improved clinical outcomes access to physicians of P3 team, tools and lead to enhanced quality focused on wellness and technology to enable shift scores and improved prevention from fee-for-service to funding to payor value-based care ➢ Individualized, ➢ Improved clinical outcomes longitudinal care plans, ➢ Physicians receive and subsequent surplus catered to the needs of financial upside from permit enhanced patient individual patient increased patient access benefits and drive faster and value created from member growth improved clinical outcomes ➢ Improved clinical outcomes and patient satisfaction at ➢ Payors benefit from no additional cost➢ Physicians retain capitated risk arrangement independence in capital- with P3 efficient, affiliate model and experience greater satisfaction The P3 Model Enables Better Patient Care, Greater Physician Satisfaction, And Enhanced Payor Growth And Cost Savings 27Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview The P3 Model Is Effective And A “Win” Scenario For All Key Stakeholders Patients Physicians Payors ➢ Improved primary care ➢ Physicians receive benefit ➢ Improved clinical outcomes access to physicians of P3 team, tools and lead to enhanced quality focused on wellness and technology to enable shift scores and improved prevention from fee-for-service to funding to payor value-based care ➢ Individualized, ➢ Improved clinical outcomes longitudinal care plans, ➢ Physicians receive and subsequent surplus catered to the needs of financial upside from permit enhanced patient individual patient increased patient access benefits and drive faster and value created from member growth improved clinical outcomes ➢ Improved clinical outcomes and patient satisfaction at ➢ Payors benefit from no additional cost➢ Physicians retain capitated risk arrangement independence in capital- with P3 efficient, affiliate model and experience greater satisfaction The P3 Model Enables Better Patient Care, Greater Physician Satisfaction, And Enhanced Payor Growth And Cost Savings 27

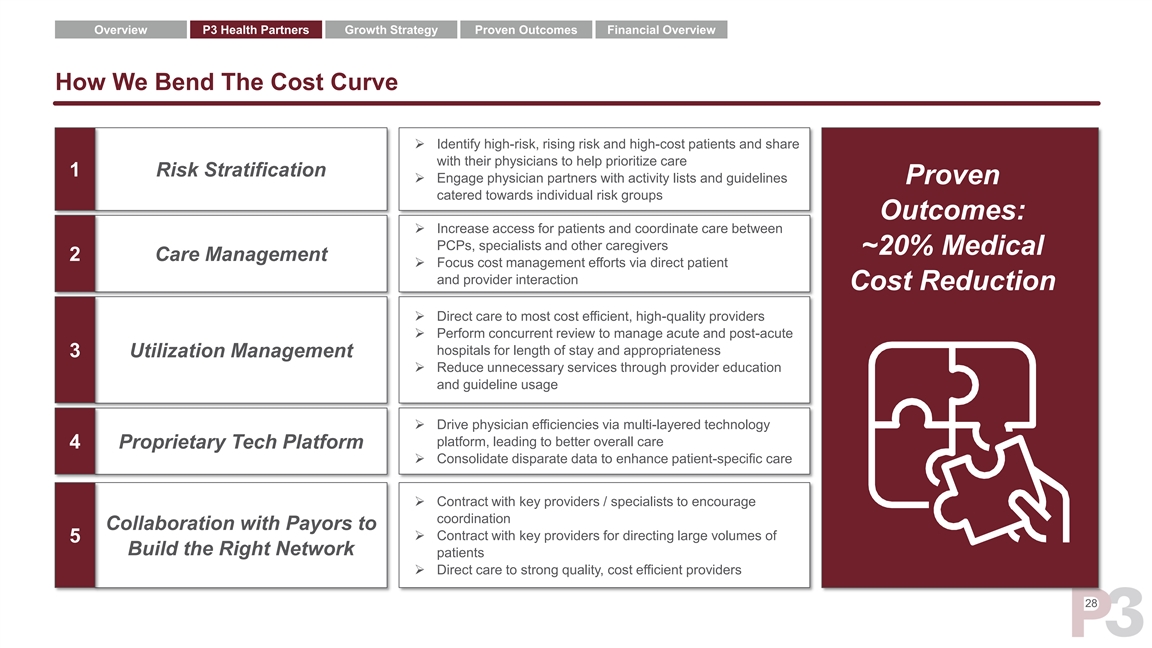

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview How We Bend The Cost Curve ➢ Identify high-risk, rising risk and high-cost patients and share with their physicians to help prioritize care 1 Risk Stratification ➢ Engage physician partners with activity lists and guidelines Proven catered towards individual risk groups Outcomes: ➢ Increase access for patients and coordinate care between PCPs, specialists and other caregivers ~20% Medical 2 Care Management ➢ Focus cost management efforts via direct patient and provider interaction Cost Reduction ➢ Direct care to most cost efficient, high-quality providers ➢ Perform concurrent review to manage acute and post-acute hospitals for length of stay and appropriateness 3 Utilization Management ➢ Reduce unnecessary services through provider education and guideline usage ➢ Drive physician efficiencies via multi-layered technology platform, leading to better overall care 4 Proprietary Tech Platform ➢ Consolidate disparate data to enhance patient-specific care ➢ Contract with key providers / specialists to encourage coordination Collaboration with Payors to ➢ Contract with key providers for directing large volumes of 5 Build the Right Network patients ➢ Direct care to strong quality, cost efficient providers 28Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview How We Bend The Cost Curve ➢ Identify high-risk, rising risk and high-cost patients and share with their physicians to help prioritize care 1 Risk Stratification ➢ Engage physician partners with activity lists and guidelines Proven catered towards individual risk groups Outcomes: ➢ Increase access for patients and coordinate care between PCPs, specialists and other caregivers ~20% Medical 2 Care Management ➢ Focus cost management efforts via direct patient and provider interaction Cost Reduction ➢ Direct care to most cost efficient, high-quality providers ➢ Perform concurrent review to manage acute and post-acute hospitals for length of stay and appropriateness 3 Utilization Management ➢ Reduce unnecessary services through provider education and guideline usage ➢ Drive physician efficiencies via multi-layered technology platform, leading to better overall care 4 Proprietary Tech Platform ➢ Consolidate disparate data to enhance patient-specific care ➢ Contract with key providers / specialists to encourage coordination Collaboration with Payors to ➢ Contract with key providers for directing large volumes of 5 Build the Right Network patients ➢ Direct care to strong quality, cost efficient providers 28

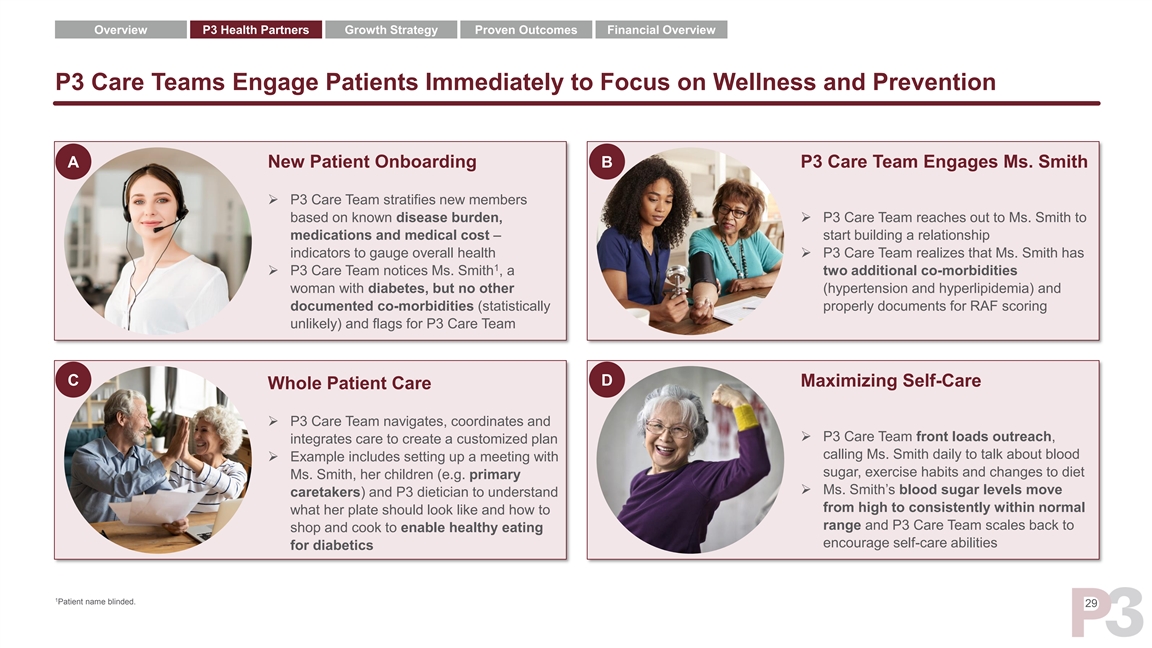

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Care Teams Engage Patients Immediately to Focus on Wellness and Prevention A New Patient Onboarding B P3 Care Team Engages Ms. Smith ➢ P3 Care Team stratifies new members based on known disease burden, ➢ P3 Care Team reaches out to Ms. Smith to medications and medical cost – start building a relationship indicators to gauge overall health➢ P3 Care Team realizes that Ms. Smith has 1 ➢ P3 Care Team notices Ms. Smith , a two additional co-morbidities woman with diabetes, but no other (hypertension and hyperlipidemia) and documented co-morbidities (statistically properly documents for RAF scoring unlikely) and flags for P3 Care Team C D Maximizing Self-Care Whole Patient Care ➢ P3 Care Team navigates, coordinates and ➢ P3 Care Team front loads outreach, integrates care to create a customized plan calling Ms. Smith daily to talk about blood ➢ Example includes setting up a meeting with sugar, exercise habits and changes to diet Ms. Smith, her children (e.g. primary ➢ Ms. Smith’s blood sugar levels move caretakers) and P3 dietician to understand from high to consistently within normal what her plate should look like and how to range and P3 Care Team scales back to shop and cook to enable healthy eating encourage self-care abilities for diabetics 1 Patient name blinded. 29Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview P3 Care Teams Engage Patients Immediately to Focus on Wellness and Prevention A New Patient Onboarding B P3 Care Team Engages Ms. Smith ➢ P3 Care Team stratifies new members based on known disease burden, ➢ P3 Care Team reaches out to Ms. Smith to medications and medical cost – start building a relationship indicators to gauge overall health➢ P3 Care Team realizes that Ms. Smith has 1 ➢ P3 Care Team notices Ms. Smith , a two additional co-morbidities woman with diabetes, but no other (hypertension and hyperlipidemia) and documented co-morbidities (statistically properly documents for RAF scoring unlikely) and flags for P3 Care Team C D Maximizing Self-Care Whole Patient Care ➢ P3 Care Team navigates, coordinates and ➢ P3 Care Team front loads outreach, integrates care to create a customized plan calling Ms. Smith daily to talk about blood ➢ Example includes setting up a meeting with sugar, exercise habits and changes to diet Ms. Smith, her children (e.g. primary ➢ Ms. Smith’s blood sugar levels move caretakers) and P3 dietician to understand from high to consistently within normal what her plate should look like and how to range and P3 Care Team scales back to shop and cook to enable healthy eating encourage self-care abilities for diabetics 1 Patient name blinded. 29

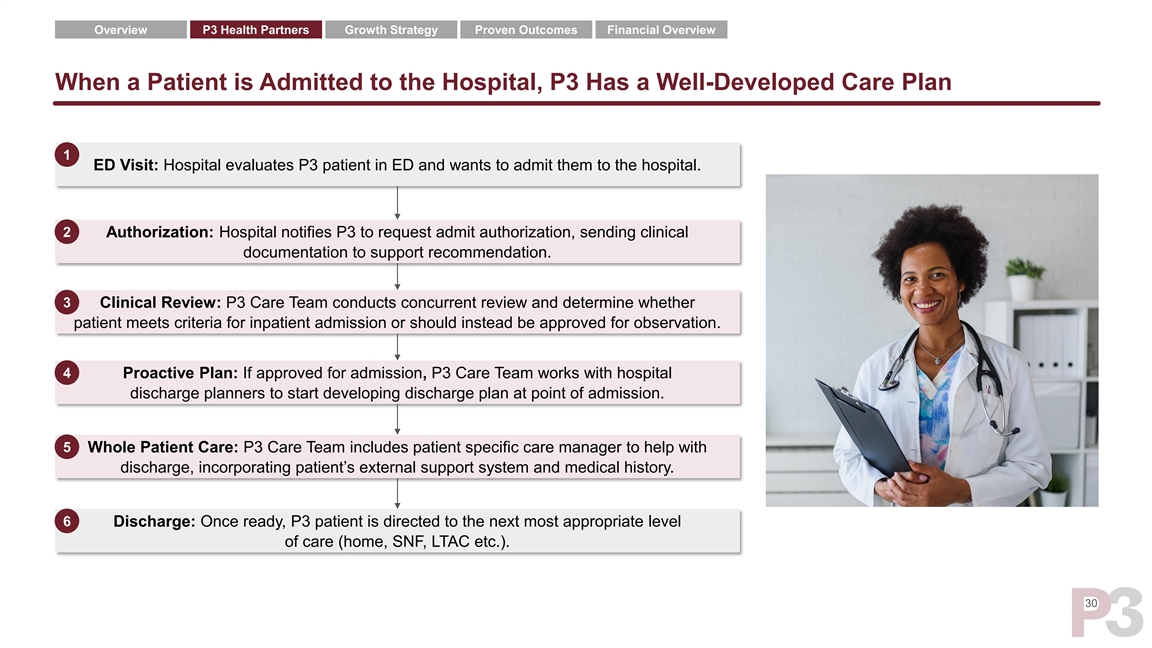

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview When a Patient is Admitted to the Hospital, P3 Has a Well-Developed Care Plan 1 ED Visit: Hospital evaluates P3 patient in ED and wants to admit them to the hospital. 2 Authorization: Hospital notifies P3 to request admit authorization, sending clinical documentation to support recommendation. 3 Clinical Review: P3 Care Team conducts concurrent review and determine whether patient meets criteria for inpatient admission or should instead be approved for observation. 4 Proactive Plan: If approved for admission, P3 Care Team works with hospital discharge planners to start developing discharge plan at point of admission. 5 Whole Patient Care: P3 Care Team includes patient specific care manager to help with discharge, incorporating patient’s external support system and medical history. 6 Discharge: Once ready, P3 patient is directed to the next most appropriate level of care (home, SNF, LTAC etc.). 30

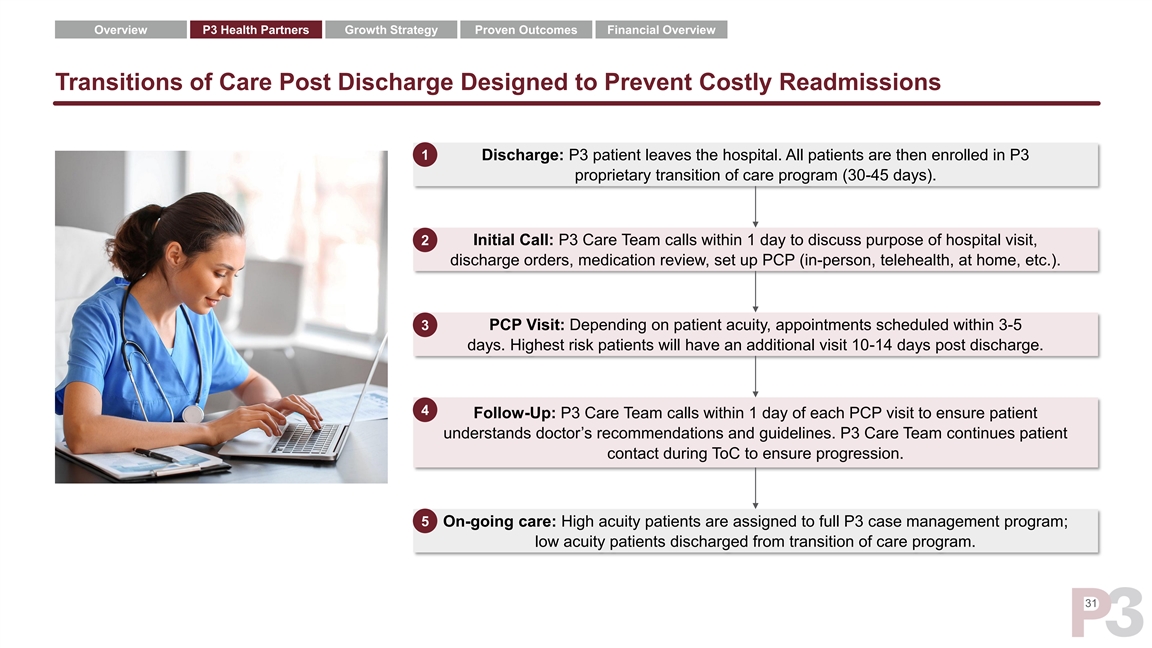

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Transitions of Care Post Discharge Designed to Prevent Costly Readmissions 1 Discharge: P3 patient leaves the hospital. All patients are then enrolled in P3 proprietary transition of care program (30-45 days). 2 Initial Call: P3 Care Team calls within 1 day to discuss purpose of hospital visit, discharge orders, medication review, set up PCP (in-person, telehealth, at home, etc.). 3 PCP Visit: Depending on patient acuity, appointments scheduled within 3-5 days. Highest risk patients will have an additional visit 10-14 days post discharge. 4 Follow-Up: P3 Care Team calls within 1 day of each PCP visit to ensure patient understands doctor’s recommendations and guidelines. P3 Care Team continues patient contact during ToC to ensure progression. 5 On-going care: High acuity patients are assigned to full P3 case management program; low acuity patients discharged from transition of care program. 31Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Transitions of Care Post Discharge Designed to Prevent Costly Readmissions 1 Discharge: P3 patient leaves the hospital. All patients are then enrolled in P3 proprietary transition of care program (30-45 days). 2 Initial Call: P3 Care Team calls within 1 day to discuss purpose of hospital visit, discharge orders, medication review, set up PCP (in-person, telehealth, at home, etc.). 3 PCP Visit: Depending on patient acuity, appointments scheduled within 3-5 days. Highest risk patients will have an additional visit 10-14 days post discharge. 4 Follow-Up: P3 Care Team calls within 1 day of each PCP visit to ensure patient understands doctor’s recommendations and guidelines. P3 Care Team continues patient contact during ToC to ensure progression. 5 On-going care: High acuity patients are assigned to full P3 case management program; low acuity patients discharged from transition of care program. 31

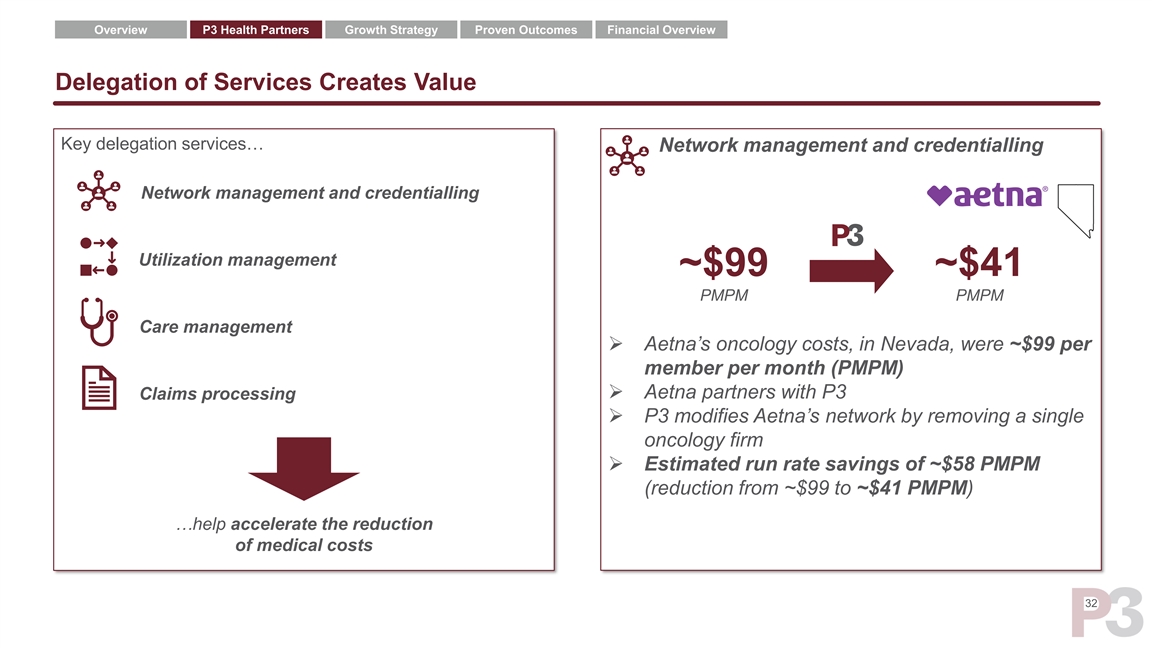

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Delegation of Services Creates Value Key delegation services… Network management and credentialling Network management and credentialling Utilization management ~$99 ~$41 PMPM PMPM Care management ➢ Aetna’s oncology costs, in Nevada, were ~$99 per member per month (PMPM) ➢ Aetna partners with P3 Claims processing ➢ P3 modifies Aetna’s network by removing a single oncology firm ➢ Estimated run rate savings of ~$58 PMPM (reduction from ~$99 to ~$41 PMPM) …help accelerate the reduction of medical costs 32Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Delegation of Services Creates Value Key delegation services… Network management and credentialling Network management and credentialling Utilization management ~$99 ~$41 PMPM PMPM Care management ➢ Aetna’s oncology costs, in Nevada, were ~$99 per member per month (PMPM) ➢ Aetna partners with P3 Claims processing ➢ P3 modifies Aetna’s network by removing a single oncology firm ➢ Estimated run rate savings of ~$58 PMPM (reduction from ~$99 to ~$41 PMPM) …help accelerate the reduction of medical costs 32

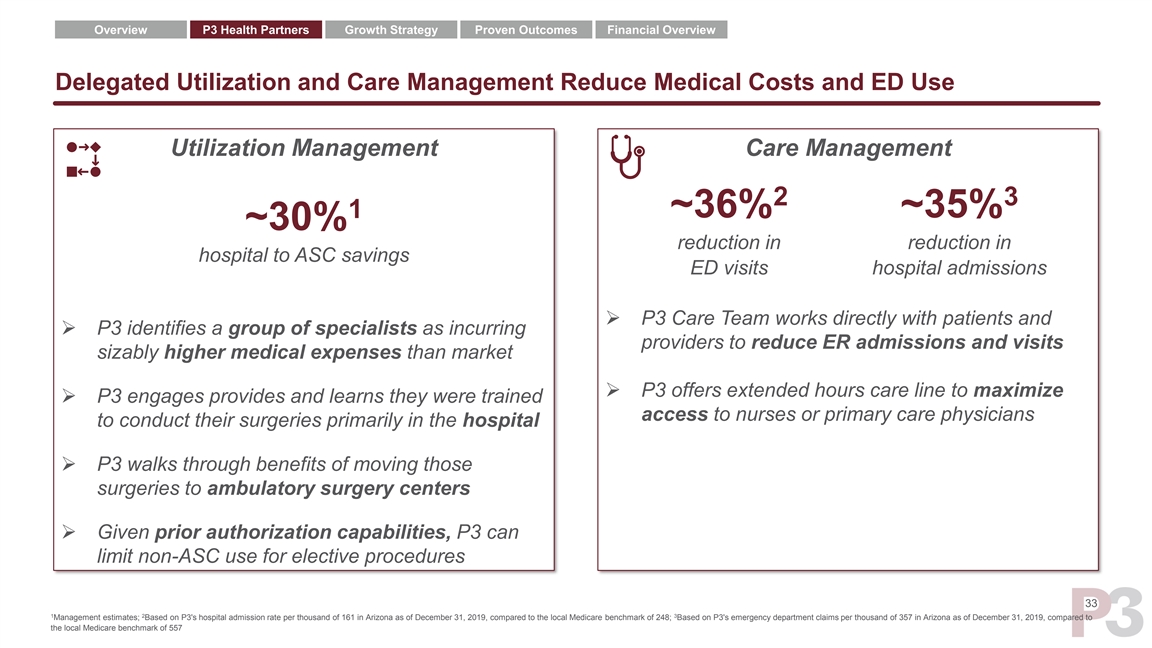

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Delegated Utilization and Care Management Reduce Medical Costs and ED Use Utilization Management Care Management 2 3 1 ~36% ~35% ~30% reduction in reduction in hospital to ASC savings ED visits hospital admissions ➢ P3 Care Team works directly with patients and ➢ P3 identifies a group of specialists as incurring providers to reduce ER admissions and visits sizably higher medical expenses than market ➢ P3 offers extended hours care line to maximize ➢ P3 engages provides and learns they were trained access to nurses or primary care physicians to conduct their surgeries primarily in the hospital ➢ P3 walks through benefits of moving those surgeries to ambulatory surgery centers ➢ Given prior authorization capabilities, P3 can limit non-ASC use for elective procedures 33 1 2 3 Management estimates; Based on P3's hospital admission rate per thousand of 161 in Arizona as of December 31, 2019, compared to the local Medicare benchmark of 248; Based on P3's emergency department claims per thousand of 357 in Arizona as of December 31, 2019, compared to the local Medicare benchmark of 557Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview Delegated Utilization and Care Management Reduce Medical Costs and ED Use Utilization Management Care Management 2 3 1 ~36% ~35% ~30% reduction in reduction in hospital to ASC savings ED visits hospital admissions ➢ P3 Care Team works directly with patients and ➢ P3 identifies a group of specialists as incurring providers to reduce ER admissions and visits sizably higher medical expenses than market ➢ P3 offers extended hours care line to maximize ➢ P3 engages provides and learns they were trained access to nurses or primary care physicians to conduct their surgeries primarily in the hospital ➢ P3 walks through benefits of moving those surgeries to ambulatory surgery centers ➢ Given prior authorization capabilities, P3 can limit non-ASC use for elective procedures 33 1 2 3 Management estimates; Based on P3's hospital admission rate per thousand of 161 in Arizona as of December 31, 2019, compared to the local Medicare benchmark of 248; Based on P3's emergency department claims per thousand of 357 in Arizona as of December 31, 2019, compared to the local Medicare benchmark of 557

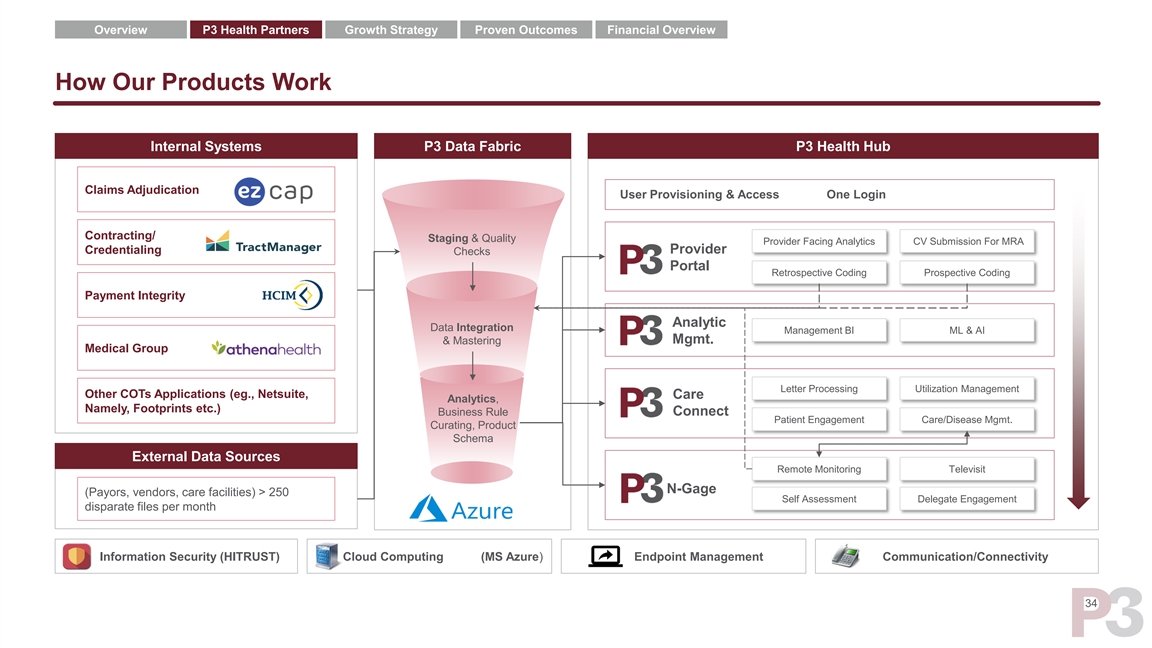

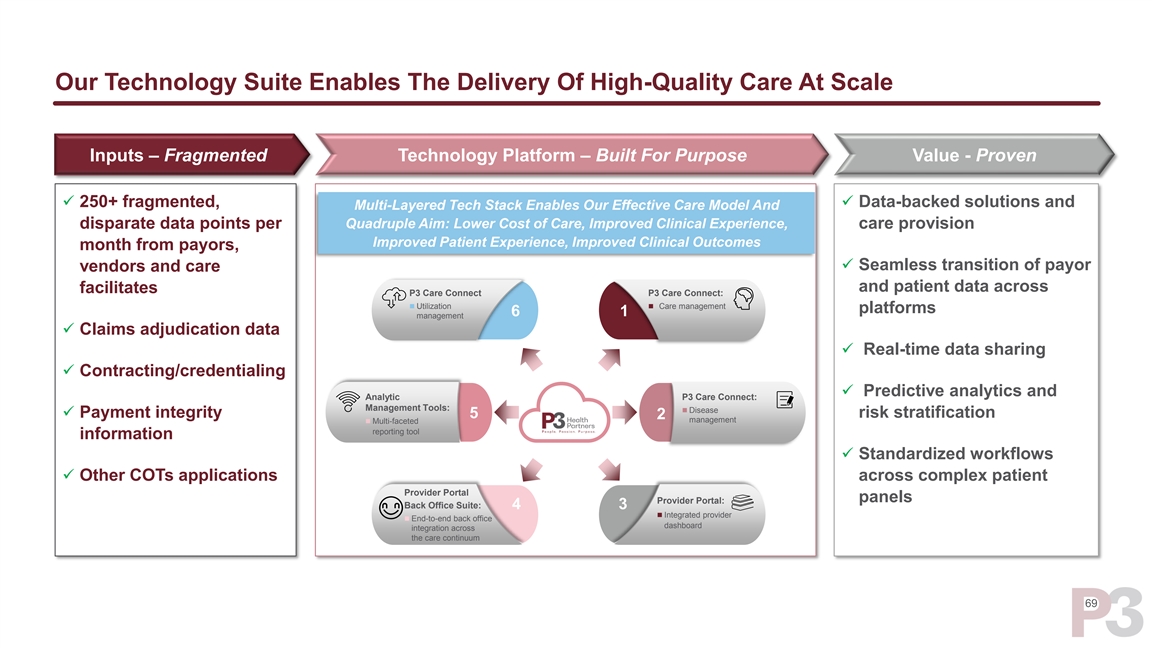

Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview How Our Products Work Internal Systems P3 Data Fabric P3 Health Hub Claims Adjudication User Provisioning & Access One Login Contracting/ Staging & Quality Provider Facing Analytics CV Submission For MRA Credentialing Provider Checks Portal Retrospective Coding Prospective Coding Payment Integrity Analytic Data Integration Management BI ML & AI & Mastering Mgmt. Medical Group Letter Processing Utilization Management Other COTs Applications (eg., Netsuite, Care Analytics, Namely, Footprints etc.) Business Rule Connect Patient Engagement Care/Disease Mgmt. Curating, Product Schema External Data Sources Remote Monitoring Televisit N-Gage (Payors, vendors, care facilities) > 250 Self Assessment Delegate Engagement disparate files per month Information Security (HITRUST) Cloud Computing (MS Azure) Endpoint Management Communication/Connectivity 34Overview P3 Health Partners Growth Strategy Proven Outcomes Financial Overview How Our Products Work Internal Systems P3 Data Fabric P3 Health Hub Claims Adjudication User Provisioning & Access One Login Contracting/ Staging & Quality Provider Facing Analytics CV Submission For MRA Credentialing Provider Checks Portal Retrospective Coding Prospective Coding Payment Integrity Analytic Data Integration Management BI ML & AI & Mastering Mgmt. Medical Group Letter Processing Utilization Management Other COTs Applications (eg., Netsuite, Care Analytics, Namely, Footprints etc.) Business Rule Connect Patient Engagement Care/Disease Mgmt. Curating, Product Schema External Data Sources Remote Monitoring Televisit N-Gage (Payors, vendors, care facilities) > 250 Self Assessment Delegate Engagement disparate files per month Information Security (HITRUST) Cloud Computing (MS Azure) Endpoint Management Communication/Connectivity 34